For unions and nonprofit organizations committed to civic engagement and economic justice, this represents a unique opportunity: mobilize borrowers in ways that align with their values, rather than against them. Messaging that highlights fairness, personal responsibility, and stewardship—core Christian principles—can resonate deeply while framing student debt as a challenge to both economic and moral accountability.

These borrowers are approaching peak voting age, meaning that engagement now could influence local and national politics in the coming election cycles. Institutions like the University of Phoenix show the scale of the opportunity: over one million borrowers owe more than $21 billion nationwide, suggesting that faith-aligned organizing strategies could have broad impact.

The strategy is clear: educate borrowers about their rights, expose predatory practices, and organize them into civic action, all while respecting their values and beliefs. Done thoughtfully, this approach can build trust and spur meaningful participation in democracy, turning a population long overlooked into an informed, motivated constituency.

The coming years will test whether unions and nonprofits seize this moment. Hundreds of thousands of conservative, Christian borrowers could become a powerful force for accountability and change—but only if engagement is value-driven, strategic, and timely.

Student loan debt has been a defining economic and political issue in the United States for over a decade. As of 2025, Americans owe nearly $1.8 trillion in student loans, with roughly 42–45 million borrowers carrying federal debt and average balances exceeding $39,000 per borrower. Delinquency rates have surged since repayment reporting resumed, with more than one in five borrowers behind on payments, and millions at risk of default. These financial pressures are now rippling through credit markets and household budgets, especially for younger, middle-aged, and lower-income borrowers. While student debt already garners public attention, shifting demographic trends and mounting economic pressures promise to reshape its political weight in the coming years unless comprehensive changes are enacted.

The largest cohort of student borrowers today consists of Millennials and older members of Generation Z, many aged between 25 and 45. These are prime years for political engagement, as individuals are more likely to vote, form households, buy homes, and shape community priorities. In 2028, this group will be even more politically active, navigating careers, families, and fiscal pressures that student debt directly influences. As borrowers age into life stages where financial stability becomes paramount, their appetite for political solutions — including forgiveness, refinancing, and more manageable repayment structures — is likely to intensify.

Student loan debt also affects communities differently. Black and Latinx borrowers are disproportionately burdened, with Black borrowers often owing more and struggling with repayment longer due to structural inequities in income and wealth. These disparities will continue to grow unless systemic reforms address not just debt levels but the economic systems that compound them over time. Communities of color are projected to constitute a larger share of the eligible electorate by 2030, and when a disproportionate share of voters in a given demographic faces an issue like unsustainable debt, it naturally becomes central to their political priorities and shapes the platforms of candidates seeking their support.

Older Americans are impacted by student loan dynamics not necessarily as borrowers themselves, but as co-signers, parents, or caregivers helping children or grandchildren manage debt. With the U.S. population aging, the 65+ age group is expected to grow as a portion of the electorate, and those over 80 will increasingly drive Medicaid and healthcare costs, adding strain to federal and state budgets. Older voters tend to vote at higher rates than younger voters, and as more families find multigenerational debt obligations weighing on retirement savings, caregiving responsibilities, and healthcare needs, the political urgency around student loan reform may expand beyond traditional “student” demographics and into older voters’ policy concerns.

Geographic and economic shifts also shape the political significance of student debt. States with high education costs, and correspondingly high average debt loads, may see student loan issues become central to local and statewide elections. Migration patterns bringing younger, more diverse populations to new regions — including parts of the South and Midwest — will likely influence electoral alignments and policy debates in competitive districts. Meanwhile, national concerns such as the growing federal debt, ongoing military engagements abroad, and rising costs associated with healthcare for an aging population amplify the stakes, creating competing pressures on policymakers who must balance debt relief against broader fiscal challenges.

Economic inequality further complicates the picture. The concentration of wealth among the richest Americans continues to grow, giving this group greater political influence and shaping policy priorities in ways that often conflict with the needs of student borrowers and middle-class families. As wealth and power accumulate at the top, voters carrying student debt may increasingly perceive systemic unfairness, heightening the political salience of debt relief and broader structural reforms. The interaction of these factors — persistent debt, rising national obligations, ongoing conflict, and economic inequality — suggests that student loans will remain intertwined with larger national debates over fiscal responsibility, social safety nets, and the distribution of economic power.

Student loan debt has already become a wedge issue in national politics, especially within Democratic primaries. The demographic shifts of the late 2020s, rising diversity, coupled economic pressures, and growing awareness of wealth inequality could make it a central concern for a broader slice of the electorate. Policymakers who ignore student debt risk alienating key voter blocs: younger voters whose turnout matters in swing states, communities of color with growing electoral influence, and middle-class families navigating financial strain alongside broader economic and geopolitical uncertainties.

The economic impact of outstanding student loan debt, from delayed homeownership to depressed small business formation, carries demographic implications that feed back into the political sphere. If current trends continue, the cost of inaction will not just be political but economic, affecting national growth rates, tax revenue, social programs, and inequality metrics that in turn shape voter sentiment and policy priorities.

Student Debt and the Shifting Political Landscape

By 2028 and into the 2030s, demographic change is poised to elevate student loan debt from a pressing public concern to a core political battleground unless policymakers act proactively. With more borrowers entering key voting blocs, disproportionate impacts across racial and economic lines, and economic consequences rippling through communities of all ages, student loan debt is more than a financial issue: it is a demographic reality shaping the future of American politics.

Sadly, the Higher Education Inquirer will not be around to cover these developments as they unfold. HEI has made predictions about student debt and its political consequences in the past, and while nothing is set in stone, the combination of rising demographics, persistent economic inequality, the mounting national debt, ongoing war-related obligations, and pressures from an aging population does not paint a promising picture. Without major policy reforms — such as targeted debt relief, changes to repayment systems, or broader higher education financing reforms — the political salience of student debt is likely to intensify, influencing campaigns, elections, and national discourse for years to come.

Sources

Education Data Initiative, “Student Loan Debt Statistics 2025,” educationdata.org TransUnion, “May 2025 Student Loan Update,” newsroom.transunion.com Forbes, “Student Loans for 64 Million Borrowers Are Heading Toward a Dangerous Cliff,” forbes.com College Board, “Trends in College Pricing and Student Aid 2025,” research.collegeboard.org LendingTree, “Student Loan Debt Statistics by State,” lendingtree.com NerdWallet, “Student Loan Debt Statistics 2025,” nerdwallet.com

The federal student loan portfolio, totaling roughly $1.6 to $1.7 trillion, is not merely an accounting entry. It is one of the largest consumer credit systems in the world and functions simultaneously as a public policy tool, a long-term revenue stream, a data infrastructure, and a political liability. It shapes who can access higher education, how risk is distributed across generations, and how the federal government exerts leverage over the postsecondary sector. Precisely because of its scale and visibility, the portfolio is uniquely vulnerable to narrative reframing.

That vulnerability was not accidental. It was constructed over decades through a series of policy decisions that stripped borrowers of normal consumer protections while preserving the financial attractiveness of student debt as an asset. Chief among these decisions was the gradual removal of bankruptcy protections for student loans. By rendering student debt effectively nondischargeable except under the narrow and punitive “undue hardship” standard, lawmakers transformed education loans into a uniquely durable financial instrument. Unlike mortgages, credit cards, or medical debt, student loans could follow borrowers for life, enforced through wage garnishment, tax refund seizure, and Social Security offsets.

This transformation made student loans exceptionally attractive for securitization. Student Loan Asset-Backed Securities, or SLABS, flourished precisely because the underlying loans were shielded from traditional credit risk. Investors could rely not on educational outcomes or borrower prosperity, but on the legal certainty that the debt would remain collectible. Even during economic downturns, SLABS were marketed as relatively stable instruments, insulated from the discharge risks that plagued other forms of consumer credit.

Private banks once dominated this market. Sallie Mae, originally a government-sponsored enterprise, became a central player in both originating and securitizing student loans, while Navient emerged as a major servicer and asset manager. Yet as Higher Education Inquirer documented in early 2025, banks ultimately lost control of student lending. Rising defaults, public outrage, state enforcement actions, and mounting evidence of predatory practices made the sector politically radioactive. The federal government stepped in not as a reformer, but as a backstop, absorbing the portfolio and stabilizing a system private finance could no longer manage without reputational and regulatory risk.

That history reveals a recurring pattern. When student lending fails in private hands, it becomes public. When the public system is allowed to fail, it becomes ripe for re-privatization.

A portfolio does not need to collapse to be declared unmanageable. It only needs to appear dysfunctional enough to justify extraordinary intervention.

The post-pandemic repayment restart, persistent servicing failures, legal challenges to income-driven repayment plans, and widespread borrower confusion have all contributed to a growing narrative of systemic breakdown. Servicers such as Maximus, operating under the Aidvantage brand, MOHELA, and others have struggled to process payments accurately, manage forgiveness programs, and provide reliable customer service. These failures are often framed as bureaucratic incompetence rather than as predictable consequences of outsourcing public functions to private contractors whose incentives are misaligned with borrower welfare.

Navient’s exit from federal servicing did not mark a retreat from the student loan ecosystem so much as a repositioning, as it continued to benefit from private loan portfolios and legacy SLABS exposure. Sallie Mae, rebranded and fully privatized, remains deeply embedded in the private student loan market, which continues to rely on the same nondischargeability framework that props up federal lending.

Crucially, these servicing failures cannot be separated from the earlier elimination of bankruptcy as a safety valve. In normal credit markets, distress is resolved through restructuring or discharge. In student lending, distress accumulates. Borrowers remain trapped, servicers remain paid, and policymakers are confronted with a swelling mass of unresolved debt that can be labeled a crisis at any politically convenient moment.

Under pyrrhic defeat theory, such a crisis is not merely tolerated. It is useful.

Once the federal portfolio is framed as broken beyond repair, the range of acceptable solutions expands. What would be politically impossible in a stable system becomes plausible in an emergency. Asset transfers, securitization of federal loans, expansion of SLABS-like instruments backed by government guarantees, or long-term conveyance of servicing and collection rights can be presented as pragmatic fixes rather than ideological choices.

A Trump administration would be particularly well positioned to exploit this dynamic. Skeptical of debt relief, hostile to administrative governance, and ideologically aligned with privatization, such an administration could recast the portfolio as a failed public experiment inherited from predecessors. In that framing, selling or offloading the portfolio is not an abdication of responsibility but an act of fiscal discipline.

Importantly, this need not take the form of an explicit, congressionally authorized sale. Risk can be shifted through securitization. Revenue streams can be monetized. Servicing authority can be extended indefinitely to private firms. Data control can migrate outside public oversight. Over time, these steps amount to de facto privatization, even if the loans remain nominally federal. The infrastructure, incentives, and profits move outward, while the political blame remains with the state.

This is where earlier McKinsey & Company studies reenter the conversation. Long before the current turmoil, McKinsey analyses identified high servicing costs, fragmented contractor oversight, weak borrower segmentation, and low political returns on administrative complexity. While framed as efficiency critiques, these studies implicitly favored market-oriented restructuring. In a crisis environment, such recommendations become blueprints for divestment.

The danger of a pyrrhic defeat strategy is that it delivers a short-term political win at the cost of long-term public capacity. Selling or functionally privatizing the student loan portfolio may improve fiscal optics, but it permanently weakens democratic control over higher education finance. Borrowers, already stripped of bankruptcy protections, lose what remains of public accountability. Policymakers lose leverage over tuition inflation and institutional behavior. The federal government relinquishes a powerful counter-cyclical tool. What remains is a debt regime optimized for extraction, enforced by servicers, securitized for investors, and detached from educational outcomes.

The defeat is real. It is borne by students, families, and future generations. The victory belongs to those who acquire distressed public assets and those who benefit ideologically from shrinking the public sphere.

Pyrrhic defeat theory reminds us that collapse is not always accidental. In the case of the federal student loan portfolio, what appears to be dysfunction or incompetence may instead be strategic surrender: a willingness to let a public system deteriorate so that it can be sold off, securitized, or outsourced under the banner of necessity. If that happens, it will not be remembered as a policy error, but as a deliberate transfer of public wealth and power—made possible by decades of legal engineering that began when bankruptcy protection was taken away and ended with student debt transformed into a permanent financial asset.

Sources

Higher Education Inquirer. “When Banks Lost Control of Student Loan Lending.” January 2025.

For Americans under 35, the term “democratic socialism” triggers neither fear nor Cold War reflexes. It represents something far simpler: a demand for a functioning society. Younger generations have grown up in a world where basic pillars of American life—higher education, medicine, economic mobility, and even life expectancy—have deteriorated while inequality has soared. Democratic socialism, in their view, is not a fringe ideology but a practical response to systems that have ceased to serve the common good.

Nowhere is this clearer than in higher education. Millennials and Gen Z entered adulthood as universities became corporate enterprises, expanding administrative layers, pushing adjunct labor to the brink, and relying on debt-financed tuition increases to keep the machine running. Public investment collapsed, predatory for-profit chains proliferated, and nonprofit universities acted like hedge funds with classrooms attached. Students saw institutions with billion-dollar endowments operate as landlords and asset managers, all while passing costs onto working families. When Bernie Sanders called for tuition-free public college, young people did not hear utopianism—they heard a plan grounded in global reality, a model that exists in Germany, Sweden, Finland, and other social democracies that treat education as a public good rather than a revenue stream.

Healthcare tells an even harsher story. Americans under 35 watched their parents and grandparents navigate a system more focused on billing codes than care, one where an ambulance ride costs a week’s wages and a bout of illness can mean bankruptcy. They experienced the rise of corporatized university medical centers, private equity–owned emergency rooms, and insurance bureaucracies that ration access more cruelly than any state. They saw life-saving drugs priced like luxury goods and mental health services pushed out of reach. Compare this to nations with universal healthcare: longer life expectancy, lower infant mortality, and far less medical debt. Again, Sanders’ Medicare for All resonated not because of ideology but because young people recognized it as a plausible path toward the kind of humane medical system described by scholars like Harriet Washington, Elisabeth Rosenthal, and Mahmud Mamdani, who all critique the structural violence embedded in systems of unequal care.

Life expectancy itself has become a generational indictment. For the first time in modern U.S. history, it has fallen, driven by overdose deaths, suicide, preventable illness, and worsening inequities. Younger Americans know that friends and peers have died far earlier than their counterparts abroad. They see that countries with strong public services—childcare, unemployment insurance, housing supports, universal healthcare—live longer, healthier lives. They also see how austerity and privatization have hollowed out public health infrastructure in the United States, leaving communities vulnerable to crises large and small. The message is clear: societies that invest in people live longer; societies that treat health as a commodity do not.

Quality of Life (QOL) ties all of this together. People under 35 face rent burdens unimaginable to previous generations, debts that prevent them from forming families, stagnant wages, and a labor market defined by precarity. They face the erosion of public space, public transit, libraries, and social supports—what Mamdani would describe as the slow unraveling of the civic realm under neoliberalism. When they look abroad, they see countries with social democratic frameworks offering guaranteed parental leave, subsidized childcare, free or nearly free college, universal healthcare, and robust worker protections. These are not distant fantasies; they are functioning models that produce higher happiness levels, stronger social trust, and more stable democracies.

Older generations often accuse young people of radicalism, but the reality is the reverse. Millennials and Gen Z are pragmatic. They have lived through the failures of unfettered capitalism: historic inequality, monopolistic industries, soaring costs of living, and a political class unresponsive to their material conditions. They have read Sanders’ critiques of oligarchy and Mamdani’s analyses of state power and structural violence, and they see themselves reflected in those diagnoses. Democratic socialism appeals because it is rooted in material improvements to daily life rather than in abstract political theory. It promises a society where income does not determine survival, where education does not require lifelong debt, where parents can afford to raise children, and where basic health is not a luxury good.

People under 35 are not afraid of democratic socialism because they have already seen what the absence of a social democratic framework produces. They are not seeking revolution for its own sake. They are seeking a livable future. And increasingly, they view democratic socialism not as a radical break but as the only realistic path toward rebuilding public institutions, revitalizing democracy, and ensuring that future generations inherit a country worth living in.

Sources

Sanders, Bernie. Our Revolution: A Future to Believe In.

Sanders, Bernie. Where We Go from Here: Two Years in the Resistance.

Mamdani, Mahmood. Define and Rule: Native as Political Identity.

Mamdani, Mahmood. Neither Settler nor Native: The Making and Unmaking of Permanent Minorities.

Washington, Harriet. Medical Apartheid.

Rosenthal, Elisabeth. An American Sickness.

Skloot, Rebecca. The Immortal Life of Henrietta Lacks.

Baldwin, Davarian. In the Shadow of the Ivory Tower.

Higher Ed Unions, Student Unions, and For-Profit College Borrowers Unite Against Trump’s “Higher Education Compact”

Several higher education unions, student unions, and former students of for-profit colleges are organizing in opposition to the Trump administration’s proposed “higher education compact”—a plan heavily shaped and promoted by private-equity billionaire Marc Rowan.

Rowan, the CEO of Apollo Global Management, has played a central role in advancing this proposal. Apollo owns several predatory for-profit institutions, including the University of Phoenix, one of the most notorious offenders in the industry.

In a recentNew York Times op-ed, Rowan took public credit for the compact, writing:

“The evidence is overwhelming: outrageous costs and prolonged indebtedness for students; poor outcomes, with too many students left unable to find meaningful work after graduating…”

Yet, under Rowan’s leadership, the University of Phoenix has become the largest source of Borrower Defense claims of any for-profit school, with more than 100,000 pending applications as of July 2025. Borrower Defense is a federal protection that allows students to seek loan forgiveness if their school misled them or violated state or federal law.

The University of Phoenix has faced multiple law enforcement investigations for deceptive recruiting tactics that targeted veterans, service members, and working adults nationwide. The school’s misconduct led to a $191 million settlement with the Federal Trade Commission for falsely claiming partnerships with major employers. More recently, the university attempted to portray itself as a public institution while seeking to sell to two states—both of which ultimately rejected the deal after public backlash.

While Rowan’s personal fortune exceeds $7 billion, borrowers continue to shoulder crushing debt from degrees that delivered little to no value. His leadership has fueled a system that profits from student harm—and now, through this compact, he is setting his sights on reshaping major public universities.

We refuse to stay silent. Borrowers, students, and educators are standing together to demand accountability and defend higher education from predatory perpetrators.

Kashana Cauley’s second novel, The Payback (out July 15, 2025), might read like a brilliantly absurd heist movie—but its critique of debt peonage, surveillance capitalism, and broken educational promises is dead serious. With its hilarious yet harrowing depiction of three underemployed retail workers taking on the student loan-industrial complex, The Payback arrives not just as a much-anticipated literary event, but as a cultural reckoning.

The protagonist, Jada Williams, is relentlessly hounded by the “Debt Police”—a dystopian twist that, while fictional, feels terrifyingly close to home for America’s 44 million student debtors. But instead of accepting a life of financial bondage, Jada and her mall coworkers hatch a plan to erase their student debt and strike back against the system that sold them a future in exchange for permanent servitude.

This wild caper—praised by Publishers Weekly, Bustle, The Boston Globe, and others for its intelligence and audacity—may be fiction, but it echoes the real-life story of one bold man who did exactly what Jada dreams of doing.

The Legend of Papas Fritas

In the mid-2000s, a Chilean man known only by his pseudonym, Papas Fritas (French Fries), pulled off one of the most radical and symbolic acts of debt resistance in modern history. A former art student at Chile’s prestigious Universidad del Mar—a private for-profit institution later shut down for corruption and fraud—Papas Fritas discovered that the university had falsified financial documents to secure millions in profits while leaving students in mountains of debt.

His response? He infiltrated the school’s administrative offices, extracted records documenting approximately $500 million in student loans, and burned them. Literally. With no backup copies.

He then turned the ashes into an art installation called “La Morada del Diablo” (The Devil’s Dwelling), displayed it publicly, and became an instant folk hero. For many Chileans, who had taken to the streets in the early 2010s protesting an exploitative and privatized higher education system, Papas Fritas was more than a trickster—he was a vigilante philosopher, an artist of revolt.

His act raised questions that still haunt us: What is the moral value of debt acquired through deception? Should the victims of predatory institutions be forced to pay for their own exploitation?

Fiction Meets Resistance

In The Payback, Cauley’s characters don’t just want debt relief—they want retribution. And like Papas Fritas, they understand that justice in an unjust system may require transgression, even sabotage. Cauley, a former Daily Show writer and incisive New York Times columnist, doesn’t shy away from this. Her prose is electric with rage, joy, absurdity, and clarity.

She also knows exactly what she’s doing. Jada’s plan to eliminate debt isn’t merely about numbers—it’s about dignity, possibility, and reclaiming a future that was sold for interest. Cauley’s fiction, like Papas Fritas’s fire, is not just a spectacle—it’s a warning, and a dare.

In an America where student debt totals over $1.7 trillion, where debt servicers act like bounty hunters, and where the promise of higher education has become a trapdoor, The Payback delivers catharsis—and inspiration.

Hollywood, take note: this story demands a screen adaptation. But more importantly, policymakers, debt collectors, and university administrators should take heed. The people are reading. And they’re getting ideas.

Preorder The Payback

Signed editions are available through Black-owned LA bookstores Reparations Club, Malik Books, and Octavia’s Bookshelf. National preorder links are now live. Read it before the Debt Police knock on your door.

Because as both Cauley and Papas Fritas remind us: sometimes, the only moral debt is the one you refuse to pay.

What happens now with the US Department of Education now that Elon Musk claims that it no longer exists? It’s hard to know yet, and even more difficult after removing career government workers that we have known for years.

We are saddened to hear of contacts we know, hard working and capable people, in an agency that has been understaffed and politicized.

We also worry for the hundreds of thousands of student loan debtors who have borrower defense to repayment claims against schools that systematically defrauded them–and have not yet received justice.

And what about all those FAFSA (financial aid) forms for students starting and continuing their schooling? How will they be processed in a timely manner?

Rachel

Oglesby most recently served as America First Policy Institute’s Chief

State Action Officer & Director, Center for the American Worker. In

this role, she worked to advance policies that promote worker freedom,

create opportunities outside of a four-year college degree, and provide

workers with the necessary skills to succeed in the modern economy, as

well as leading all of AFPI’s state policy development and advocacy

work. She previously worked as Chief of Policy and Deputy Chief of Staff

for Governor Kristi Noem in South Dakota, overseeing the implementation

of the Governor’s pro-freedom agenda across all policy areas and state

government agencies. Oglesby holds a master’s degree in public policy

from George Mason University and earned her bachelor’s degree in

philosophy from Wake Forest University.

Jonathan Pidluzny – Deputy Chief of Staff for Policy and Programs

Jonathan

Pidluzny most recently served as Director of the Higher Education

Reform Initiative at the America First Policy Institute. Prior to that,

he was Vice President of Academic Affairs at the American Council of

Trustees and Alumni, where his work focused on academic freedom and

general education. Jonathan began his career in higher education

teaching political science at Morehead State University, where he was an

associate professor, program coordinator, and faculty regent from

2017-2019. He received his Ph.D from Boston College and holds a

bachelor’s degree and master’s degree from the University of Alberta.

Chase Forrester – Deputy Chief of Staff for Operations

Virginia

“Chase” Forrester most recently served as the Chief Events Officer at America First Policy Institute, where she oversaw the planning and

execution of 80+ high-profile events annually for AFPI’s 22 policy

centers, featuring former Cabinet Officials and other distinguished

speakers. Chase previously served as Operations Manager on the

Trump-Pence 2020 presidential campaign, where she spearheaded all event

operations for the Vice President of the United States and the Second

Family. Chase worked for the National Republican Senatorial Committee

during the Senate run-off races in Georgia and as a fundraiser for

Members of Congress. Chase graduated from Clemson University with a

bachelor’s degree in political science and a double-minor in Spanish and

legal studies.

Steve Warzoha – White House Liaison

Steve

Warzoha joins the U.S. Department of Education after most recently

serving on the Trump-Vance Transition Team. A native of Greenwich, CT,

he is a former local legislator who served on the Education Committee

and as Vice Chairman of both the Budget Overview and Transportation

Committees. He is also an elected leader of the Greenwich Republican

Town Committee. Steve has run and served in senior positions on numerous

local, state, and federal campaigns. Steve comes from a family of

educators and public servants and is a proud product of Greenwich Public

Schools and an Eagle Scout.

Tom Wheeler – Principal Deputy General Counsel

Tom

Wheeler’s prior federal service includes as the Acting Assistant

Attorney General for Civil Rights at the U.S. Department of Justice, a

Senior Advisor to the White House Federal Commission on School Safety,

and as a Senior Advisor/Counsel to the Secretary of Education. He has

also been asked to serve on many Boards and Commissions, including as

Chair of the Hate Crimes Sub-Committee for the Federal Violent Crime

Reduction Task Force, a member of the Department of Justice’s Regulatory

Reform Task Force, and as an advisor to the White House Coronavirus

Task Force, where he worked with the CDC and HHS to develop guidelines

for the safe reopening of schools and guidelines for law enforcement and

jails/prisons. Prior to rejoining the U.S. Department of Education, Tom

was a partner at an AM-100 law firm, where he represented federal,

state, and local public entities including educational institutions and

law enforcement agencies in regulatory, administrative, trial, and

appellate matters in local, state and federal venues. He is a frequent

author and speaker in the areas of civil rights, free speech, and

Constitutional issues, improving law enforcement, and school safety.

Craig Trainor – Deputy Assistant Secretary for Policy, Office for Civil Rights

Craig

Trainor most recently served as Senior Special Counsel with the U.S.

House of Representatives Committee on the Judiciary under Chairman Jim

Jordan (R-OH), where Mr. Trainor investigated and conducted oversight of

the U.S. Department of Justice, including its Civil Rights Division,

the FBI, the Biden-Harris White House, and the Intelligence Community

for civil rights and liberties abuses. He also worked as primary counsel

on the House Judiciary’s Subcommittee on the Constitution and Limited

Government’s investigation into the suppression of free speech and

antisemitic harassment on college and university campuses, resulting in

the House passing the Antisemitism Awareness Act of 2023. Previously, he

served as Senior Litigation Counsel with the America First Policy

Institute under former Florida Attorney General Pam Bondi, Of Counsel

with the Fairness Center, and had his own civil rights and criminal

defense law practice in New York City for over a decade. Upon graduating

from the Catholic University of America, Columbus School of Law, he

clerked for Chief Judge Frederick J. Scullin, Jr., U.S. District Court

for the Northern District of New York. Mr. Trainor is admitted to

practice law in the state of New York, the U.S. District Court for the

Southern and Eastern Districts of New York, and the U.S. Supreme Court.

Madi Biedermann – Deputy Assistant Secretary, Office of Communications and Outreach

Madi

Biedermann is an experienced education policy and communications

professional with experience spanning both federal and state government

and policy advocacy organizations. She most recently worked as the Chief

Operating Officer at P2 Public Affairs. Prior to that, she served as an Assistant Secretary of Education for Governor Glenn Youngkin and worked

as a Special Assistant and Presidential Management Fellow at the Office

of Management and Budget in the first Trump Administration. Madi

received her bachelor’s degree and master of public administration from

the University of Southern California.

Candice Jackson – Deputy General Counsel

Candice

Jackson returns to the U.S. Department of Education to serve as Deputy

General Counsel. Candice served in the first Trump Administration as

Acting Assistant Secretary for Civil Rights, and Deputy General Counsel,

from 2017-2021. For the last few years, Candice has practiced law in

Washington State and California and consulted with groups and

individuals challenging the harmful effects of the concept of “gender

identity” in laws and policies in schools, employment, and public

accommodations. Candice is mom to girl-boy twins Madelyn and Zachary,

age 11.

Joshua Kleinfeld – Deputy General Counsel

Joshua

Kleinfeld is the Allison & Dorothy Rouse Professor of Law and

Director of the Boyden Gray Center for the Study of the Administrative

State at George Mason University’s Scalia School of Law. He writes and

teaches about constitutional law, criminal law, and statutory

interpretation, focusing in all fields on whether democratic ideals are

realized in governmental practice. As a scholar and public intellectual,

he has published work in the Harvard, Stanford, and University of

Chicago Law Reviews, among other venues. As a practicing lawyer, he has

clerked on the D.C. Circuit, Fourth Circuit, and Supreme Court of

Israel, represented major corporations accused of billion-dollar

wrongdoing, and, on a pro bono basis, represented children accused of

homicide. As an academic, he was a tenured full professor at

Northwestern Law School before lateraling to Scalia Law School. He holds

a J.D. in law from Yale Law School, a Ph.D. in philosophy from the

Goethe University of Frankfurt, and a B.A. in philosophy from Yale

College.

Hannah Ruth Earl – Director, Center for Faith-Based and Neighborhood Partnerships

Hannah

Ruth Earl is the former executive director of America’s Future, where

she cultivated communities of freedom-minded young professionals and

local leaders. She previously co-produced award-winning feature films as

director of talent and creative development at the Moving Picture

Institute. A native of Tennessee, she holds a master of arts in religion

from Yale Divinity School.

When

borrowers default on their federal student loans, the U.S. Department

of Education (“Department of Education”) can collect the outstanding

balance through forced collections, including the offset of tax refunds

and Social Security benefits and the garnishment of wages. At the

beginning of the COVID-19 pandemic, the Department of Education paused

collections on defaulted federal student loans.

This year, collections are set to resume and almost 6 million student

loan borrowers with loans in default will again be subject to the

Department of Education’s forced collection of their tax refunds, wages,

and Social Security benefits.

Among the borrowers who are likely to experience forced collections are

an estimated 452,000 borrowers ages 62 and older with defaulted loans

who are likely receiving Social Security benefits.

This

spotlight describes the circumstances and experiences of student loan

borrowers affected by the forced collection of Social Security benefits.

It also describes how forced collections can push older borrowers into

poverty, undermining the purpose of the Social Security program.

Key findings

The

number of Social Security beneficiaries experiencing forced collection

grew by more than 3,000 percent in fewer than 20 years; the count is

likely to grow as the age of student loan borrowers trends older.

Between 2001 and 2019, the number of Social Security beneficiaries

experiencing reduced benefits due to forced collection increased from

approximately 6,200 to 192,300. This exponential growth is likely driven

by older borrowers who make up an increasingly large share of the

federal student loan portfolio. The number of student loan borrowers

ages 62 and older increased by 59 percent from 1.7 million in 2017 to

2.7 million in 2023, compared to a 1 percent decline among borrowers

under the age of 62.

The total amount

of Social Security benefits the Department of Education collected

between 2001 and 2019 through the offset program increased from $16.2

million to $429.7 million. Despite the exponential increase in

collections from Social Security, the majority of money the Department

of Education has collected has been applied to interest and fees and has

not affected borrowers’ principal amount owed. Furthermore, between

2016 and 2019, the Department of the Treasury’s fees alone accounted for

nearly 10 percent of the average borrower’s lost Social Security

benefits.

More than one in three

Social Security recipients with student loans are reliant on Social

Security payments, meaning forced collections could significantly

imperil their financial well-being. Approximately 37 percent of the

1.3 million Social Security beneficiaries with student loans rely on

modest payments, an average monthly benefit of $1,523, for 90 percent of

their income. This population is particularly vulnerable to reduction

in their benefits especially if benefits are offset year-round. In 2019,

the average annual amount collected from individual beneficiaries was

$2,232 ($186 per month).

The physical well-being of half of Social Security beneficiaries with student loans in default may be at risk.

Half of Social Security beneficiaries with student loans in default and

collections skipped a doctor’s visit or did not obtain prescription

medication due to cost.

Existing minimum income protections fail to protect student loan borrowers with Social Security against financial hardship.

Currently, only $750 per month of Social Security income—an amount that

is $400 below the monthly poverty threshold for an individual and has

not been adjusted for inflation since 1996—is protected from forced

collections by statute. Even if the minimum protected income was

adjusted for inflation, beneficiaries would likely still experience

hardship, such as food insecurity and problems paying utility bills. A

higher threshold could protect borrowers against hardship more

effectively. The CFPB found that for 87 percent of student loan

borrowers who receive Social Security, their benefit amount is below 225

percent of the federal poverty level (FPL), an income level at which

people are as likely to experience material hardship as those with

incomes below the federal poverty level.

Large

shares of Social Security beneficiaries affected by forced collections

may be eligible for relief or outright loan cancellation, yet they are

unable to access these benefits, possibly due to insufficient

automation or borrowers’ cognitive and physical decline. As many as

eight in ten Social Security beneficiaries with loans in default may be

eligible to suspend or reduce forced collections due to financial

hardship. Moreover, one in five Social Security beneficiaries may be

eligible for discharge of their loans due to a disability. Yet these

individuals are not accessing such relief because the Department of

Education’s data matching process insufficiently identifies those who

may be eligible.

Taken together,

these findings suggest that the Department of Education’s forced

collections of Social Security benefits increasingly interfere with

Social Security’s longstanding purpose of protecting its beneficiaries

from poverty and financial instability.

Introduction

When

borrowers default on their federal student loans, the Department of

Education can collect the outstanding balance through forced

collections, including the offset of tax refunds and Social Security

benefits, and the garnishment of wages. At the beginning of the COVID-19

pandemic, the Department of Education paused collections on defaulted

federal student loans. This year, collections are set to resume and

almost 6 million student loan borrowers with loans in default will again

be subject to the Department of Education’s forced collection of their

tax refunds, wages, and Social Security benefits.

Among

the borrowers who are likely to experience the Department of

Education’s renewed forced collections are an estimated 452,000

borrowers with defaulted loans who are ages 62 and older and who are

likely receiving Social Security benefits.

Congress created the Social Security program in 1935 to provide a basic

level of income that protects insured workers and their families from

poverty due to situations including old age, widowhood, or disability.

The Social Security Administration calls the program “one of the most

successful anti-poverty programs in our nation’s history.”

In 2022, Social Security lifted over 29 million Americans from poverty,

including retirees, disabled adults, and their spouses and dependents.

Congress has recognized the importance of securing the value of Social

Security benefits and on several occasions has intervened to protect

them.

This

spotlight describes the circumstances and experiences of student loan

borrowers affected by the forced collection of their Social Security

benefits.

It also describes how the purpose of Social Security is being

increasingly undermined by the limited and deficient options the

Department of Education has to protect Social Security beneficiaries

from poverty and hardship.

The forced collection of Social Security benefits has increased exponentially.

Federal

student loans enter default after 270 days of missed payments and

transfer to the Department of Education’s default collections program

after 360 days. Borrowers with a loan in default face several

consequences: (1) their credit is negatively affected; (2) they lose

eligibility to receive federal student aid while their loans are in

default; (3) they are unable to change repayment plans and request

deferment and forbearance; and (4) they face forced collections of tax refunds, Social Security benefits, and wages among other payments.

To conduct its forced collections of federal payments like tax refunds

and Social Security benefits, the Department of Education relies on a

collection service run by the U.S. Department of the Treasury called the

Treasury Offset Program.

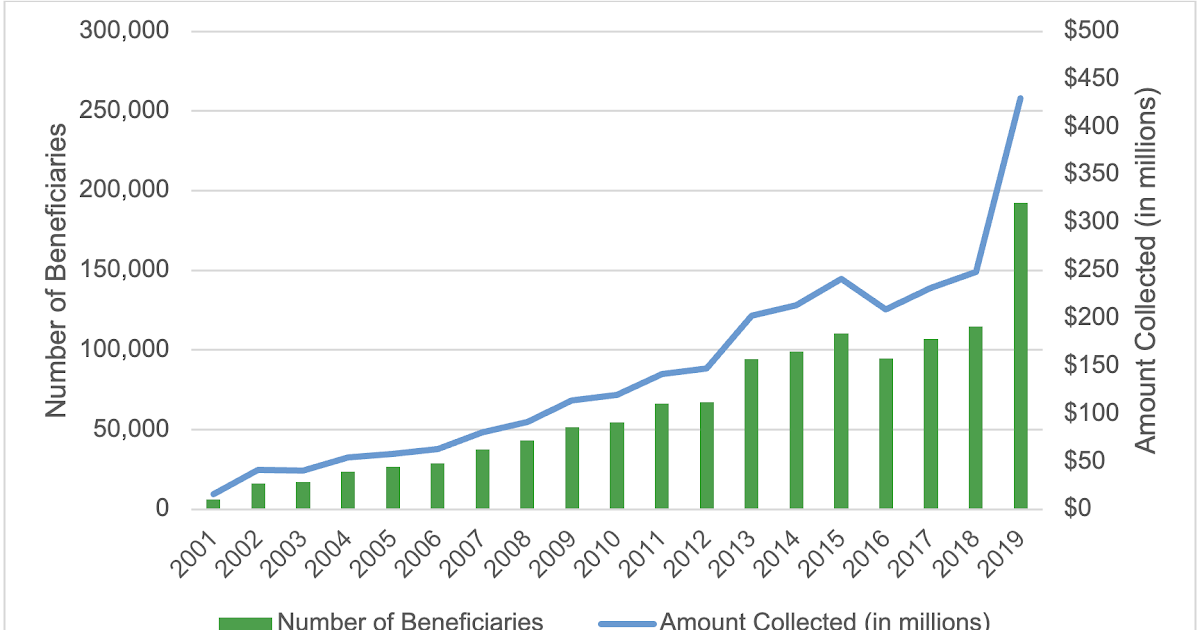

Between

2001 and 2019, the number of student loan borrowers facing forced

collection of their Social Security benefits increased from at least

6,200 to 192,300.

That is a more than 3,000 percent increase in fewer than 20 years. By

comparison, the number of borrowers facing forced collections of their

tax refunds increased by about 90 percent from 1.17 million to 2.22

million during the same period.

This exponential growth of Social Security offsets between 2001 and 2019 is likely driven by multiple factors including:

Older

borrowers accounted for an increasingly large share of the federal

student loan portfolio due to increasing average age of enrollment and

length of time in repayment. Data from the Department of Education

(which is only available since 2017), show that the number of student

loan borrowers ages 62 and older, increased 24 percent from 1.7 million

in 2017 to 2.1 million in 2019, compared to less than 1 percent among

borrowers under the age of 62.

A larger number of borrowers, especially older borrowers, had loans in default.

Data from the Department of Education show that the number of student

loan borrowers with a defaulted loan increased by 230 percent from 3.8

million in 2006 to 8.8 million in 2019. Compounding these trends is the fact that older borrowers are twice as likely to have a loan in default than younger borrowers.

Due

to these factors, the total amount of Social Security benefits the

Department of Education collected between 2001 and 2019 through the

offset program increased annually from $16.2 million to $429.7 million

(when adjusted for inflation).

This increase occurred even though the average monthly amount the

Department of Education collected from individual beneficiaries was the

same for most years, at approximately $180 per month.

Figure 1: Number of Social Security beneficiaries and total amount collected for student loans (2001-2019)

Source: CFPB analysis of public data from U.S. Treasury’s Fiscal Data portal. Amounts are presented in 2024 dollars.

While the total collected from

Social Security benefits has increased exponentially, the majority of

money the Department of Education collected has not been applied to

borrowers’ principal amount owed. Specifically, nearly three-quarters of

the monies the Department of Education collects through offsets is

applied to interest and fees, and not towards paying down principal

balances.

Between 2016 and 2019, the U.S. Department of the Treasury charged the

Department of Education between $13.12 and $15.00 per Social Security

offset, or approximately between $157.44 and $180 for 12 months of

Social Security offsets per beneficiary with defaulted federal student

loans. As a matter of practice, the Department of Education often passes these fees on directly to borrowers.

Furthermore, these fees accounted for nearly 10 percent of the average

monthly borrower’s lost Social Security benefits which was $183 during

this time.

Interest and fees not only reduce beneficiaries’ monthly benefits, but

also prolong the period that beneficiaries are likely subject to forced

collections.

Forced collections are compromising Social Security beneficiaries’ financial well-being.

Forced

collection of Social Security benefits affects the financial well-being

of the most vulnerable borrowers and can exacerbate any financial and

health challenges they may already be experiencing. The CFPB’s analysis

of the Survey of Income and Program Participation (SIPP) pooled data for

2018 to 2021 finds that Social Security beneficiaries with student

loans receive an average monthly benefit of $1,524.

The analysis also indicates that approximately 480,000 (37 percent) of

the 1.3 million beneficiaries with student loans rely on these modest

payments for 90 percent or more of their income,

thereby making them particularly vulnerable to reduction in their

benefits especially if benefits are offset year-round. In 2019, the

average annual amount collected from individual beneficiaries was $2,232

($186 per month).

A

recent survey from The Pew Charitable Trusts found that more than nine

in ten borrowers who reported experiencing wage garnishment or Social

Security payment offsets said that these penalties caused them financial

hardship.

Consequently, for many, their ability to meet their basic needs,

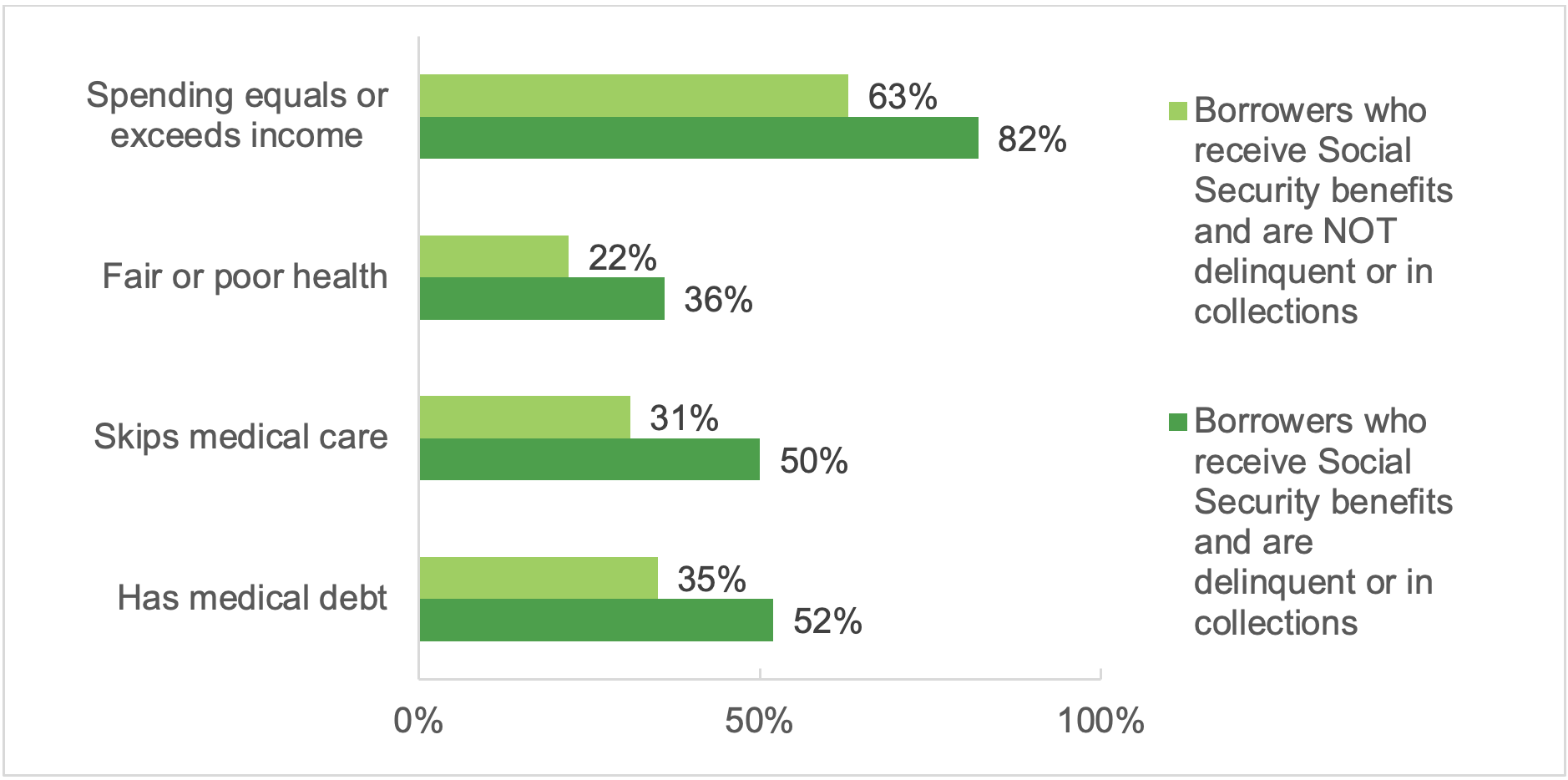

including access to healthcare, became more difficult. According to our

analysis of the Federal Reserve’s Survey of Household Economic and

Decision-making (SHED), half of Social Security beneficiaries with

defaulted student loans skipped a doctor’s visit and/or did not obtain

prescription medication due to cost.

Moreover, 36 percent of Social Security beneficiaries with loans in

delinquency or in collections report fair or poor health. Over half of

them have medical debt.

Figure 2: Selected financial experiences and hardships among subgroups of loan borrowers

Source: CFPB analysis of the Federal Reserve Board Survey of Household Economic and Decision-making (2019-2023).

Social Security recipients

subject to forced collection may not be able to access key public

benefits that could help them mitigate the loss of income. This is

because Social Security beneficiaries must list the unreduced amount of

their benefits prior to collections when applying for other means-tested

benefits programs such as Social Security Insurance (SSI), Supplemental

Nutrition Assistance Program (SNAP), and the Medicare Savings Programs.

Consequently, beneficiaries subject to forced collections must report

an inflated income relative to what they are actually receiving. As a

result, these beneficiaries may be denied public benefits that provide

food, medical care, prescription drugs, and assistance with paying for

other daily living costs.

Consumers’

complaints submitted to the CFPB describe the hardship caused by forced

collections on borrowers reliant on Social Security benefits to pay for

essential expenses.

Consumers often explain their difficulty paying for such expenses as

rent and medical bills. In one complaint, a consumer noted that they

were having difficulty paying their rent since their Social Security

benefit usually went to paying that expense.

In another complaint, a caregiver described that the money was being

withheld from their mother’s Social Security, which was the only source

of income used to pay for their mother’s care at an assisted living

facility.

As forced collections threaten the housing security and health of

Social Security beneficiaries, they also create a financial burden on

non-borrowers who help address these hardships, including family members

and caregivers.

Existing minimum income protections fail to protect student loan borrowers with Social Security against financial hardship.

The

Debt Collection Improvement Act set a minimum floor of income below

which the federal government cannot offset Social Security benefits and

subsequent Treasury regulations established a cap on the percentage of

income above that floor.

Specifically, these statutory guardrails limit collections to 15

percent of Social Security benefits above $750. The minimum threshold

was established in 1996 and has not been updated since. As a result, the

amount protected by law alone does not adequately protect beneficiaries

from financial hardship and in fact no longer protects them from

falling below the federal poverty level (FPL). In 1996, $750 was nearly

$100 above the monthly poverty threshold for an individual.

Today that same protection is $400 below the threshold. If the

protected amount of $750 per month ($9,000 per year) set in 1996 was

adjusted for inflation, in 2024 dollars, it would total $1,450 per month

($17,400 per year).

Figure

3: Comparison of monthly FPL threshold with the current protected

amount established in 1996 and the amount that would be protected with

inflation adjustment

Source: Calculations by the CFPB. Notes: Inflation adjustments based on the consumer price index (CPI).

Even if the minimum protected

income of $750 is adjusted for inflation, beneficiaries will likely

still experience hardship as a result of their reduced benefits.

Consumers with incomes above the poverty line also commonly experience

material hardship. This suggests that a threshold that is higher than the poverty level will more effectively protect against hardship.

Indeed, in determining an income threshold for $0 payments under the

SAVE plan, the Department of Education researchers used material

hardship (defined as being unable to pay utility bills and reporting

food insecurity) as their primary metric, and found similar levels of

material hardship among those with incomes below the poverty line and

those with incomes up to 225 percent of the FPL.

Similarly, the CFPB’s analysis of a pooled sample of SIPP respondents

finds the same levels of material hardship for Social Security

beneficiaries with student loans with incomes below 100 percent of the

FPL and those with incomes up to 225 percent of the FPL.

The CFPB found that for 87 percent of student loan borrowers who

receive Social Security, their benefit amount is below 225 percent of

the FPL.

Accordingly, all of those borrowers would be removed from forced

collections if the Department of Education applied the same income

metrics it established under the SAVE program to an automatic hardship

exemption program.

Existing options for relief from forced collections fail to reach older borrowers.

Borrowers

with loans in default remain eligible for certain types of loan

cancellation and relief from forced collections. However, our analysis

suggests that these programs may not be reaching many eligible

consumers. When borrowers do not benefit from these programs, their

hardship includes, but is not limited to, unnecessary losses to their

Social Security benefits and negative credit reporting.

Borrowers who become disabled after reaching full retirement age may miss out on Total and Permanent Disability

The

Total and Permanent Disability (TPD) discharge program cancels federal

student loans and effectively stops all forced collections for disabled

borrowers who meet certain requirements. After recent revisions to the

program, this form of cancelation has become common for those borrowers

with Social Security who became disabled prior to full retirement age. In 2016, a GAO study documented the significant barriers to TPD that Social Security beneficiaries faced.

To address GAO’s concerns, the Department of Education in 2021 took a

series of mitigating actions, including entering into a data-matching

agreement with the Social Security Administration (SSA) to automate the

TPD eligibility determination and discharge process.

This process was expanded further with new final rules being

implemented July 1, 2023 that expanded the categories of borrowers

eligible for automatic TPD cancellation. In total, these changes successfully resulted in loan cancelations for approximately 570,000 borrowers.

However,

the automation and other regulatory changes did not significantly

change the application process for consumers who become disabled after

they reach full retirement age or who have already claimed the Social

Security retirement benefits. For these beneficiaries, because they are

already receiving retirement benefits, SSA does not need to determine

disability status. Likewise, SSA does not track disability status for

those individuals who become disabled after they start collecting their

Social Security retirement benefits.

Consequently,

SSA does not transfer information on disability to the Department of

Education once the beneficiary begins collecting Social Security

retirement.

These individuals therefore will not automatically get a TPD discharge

of their student loans, and they must be aware and physically and

mentally able to proactively apply for the discharge.

The

CFPB’s analysis of the Census survey data suggests that the population

that is excluded from the TPD automation process could be substantial.

More than one in five (22 percent) Social Security beneficiaries with

student loans are receiving retirement benefits and report a disability

such as a limitation with vision, hearing, mobility, or cognition.

People with dementia and other cognitive disabilities are among those

with the greatest risk of being excluded, since they are more likely to

be diagnosed after the age 70, which is the maximum age for claiming

retirement benefits.

These

limitations may also help explain why older borrowers are less likely

to rehabilitate their defaulted student loans. Specifically, 11 percent

of student loan borrowers ages 50 to 59 facing forced collections

successfully rehabilitated their loans, while only five percent of borrowers over the age of 75 do so.

Figure

4: Number of student loan borrowers ages 50 and older in forced

collection, borrowers who signed a rehabilitation agreement, and

borrowers who successfully rehabilitated a loan by selected age groups

Age Group

Number of Borrowers in Offset

Number of Borrowers Who Signed a Rehabilitation Agreement

Percent of Borrowers Who Signed a Rehabilitation Agreement

Number of Borrowers Successfully Rehabilitated

Percent of Borrowers who Successfully Rehabilitated

50 to 59

265,200

50,800

14%

38,400

11%

60 to 74

184,900

24,100

11%

18,500

8%

75 and older

15,800

1,000

6%

800

5%

Source: CFPB analysis of data provided by the Department of Education.

Shifting demographics of

student loan borrowers suggest that the current automation process may

become less effective to protect Social Security benefits from forced

collections as more and more older adults have student loan debt. The

fastest growing segment of student loan borrowers are adults ages 62 and

older. These individuals are generally eligible for retirement

benefits, not disability benefits, because they cannot receive both

classifications at the same time. Data from the Department of Education

reflect that the number of student loan borrowers ages 62 and older

increased by 59 percent from 1.7 million in 2017 to 2.7 million in 2023.

In comparison, the number of borrowers under the age of 62 remained

unchanged at 43 million in both years.

Furthermore, additional data provided to the CFPB by the Department of

Education show that nearly 90,000 borrowers ages 81 and older hold an

average amount of $29,000 in federal student loan debt, a substantial

amount despite facing an estimated average life expectancy of less than

nine years.

Existing exceptions to forced collections fail to protect many Social Security beneficiaries

In

addition to TPD discharge, the Department of Education offers reduction

or suspension of Social Security offset where borrowers demonstrate

financial hardship.

To show hardship, borrowers must provide documentation of their income

and expenses, which the Department of Education then uses to make its

determination.

Unlike the Debt Collection Improvement Act’s minimum protections, the

eligibility for hardship is based on a comparison of an individual’s

documented income and qualified expenses. If the borrower has eligible

monthly expenses that exceed or match their income, the Department of

Education then grants a financial hardship exemption.

The

CFPB’s analysis suggests that the vast majority of Social Security

beneficiaries with student loans would qualify for a hardship

protection. According to CFPB’s analysis of the Federal Reserve Board’s

SHED, eight in ten (82 percent) of Social Security beneficiaries with

student loans in default report that their expenses equal or exceed

their income.

Accordingly, these individuals would likely qualify for a full

suspension of forced collections. Yet the GAO found that in 2015 (when

the last data was available) less than ten percent of Social Security

beneficiaries with forced collections applied for a hardship exemption

or reduction of their offset.

A possible reason for the low uptake rate is that many beneficiaries or

their caregivers never learn about the hardship exemption or the

possibility of a reduction in the offset amount.

For those that do apply, only a fraction get relief. The GAO study

found that at the time of their initial offset, only about 20 percent of

Social Security beneficiaries ages 50 and older with forced collections

were approved for a financial hardship exemption or a reduction of the

offset amount if they applied.

Conclusion

As

hundreds of thousands of student loan borrowers with loans in default

face the resumption of forced collection of their Social Security

benefits, this spotlight shows that the forced collection of Social

Security benefits causes significant hardship among affected borrowers.

The spotlight also shows that the basic income protections aimed at

preventing poverty and hardship among affected borrowers have become

increasingly ineffective over time. While the Department of Education

has made some improvements to expand access to relief options,

especially for those who initially receive Social Security due to a

disability, these improvements are insufficient to protect older adults

from the forced collection of their Social Security benefits.

Taken

together, these findings suggest that forced collections of Social

Security benefits increasingly interfere with Social Security’s

longstanding purpose of protecting its beneficiaries from poverty and

financial instability. These findings also suggest that alternative

approaches are needed to address the harm that forced collections cause

on beneficiaries and to compensate for the declining effectiveness of

existing remedies. One potential solution may be found in the Debt

Collection Improvement Act, which provides that when forced collections

“interfere substantially with or defeat the purposes of the payment

certifying agency’s program” the head of an agency may request from the

Secretary of the Treasury an exemption from forced collections.

Given the data findings above, such a request for relief from the

Commissioner of the Social Security Administration on behalf of Social

Security beneficiaries who have defaulted student loans could be

justified. Unless the toll of forced collections on Social Security

beneficiaries is considered alongside the program’s stated goals, the

number of older adults facing these challenges is only set to grow.

Data and Methodology

To

develop this report, the CFPB relied primarily upon original analysis

of public-use data from the U.S. Census Bureau Survey of Income and

Program Participation (SIPP), the Federal Reserve Board Board’s Survey

of Household Economics and Decision-making (SHED), U.S. Department of

the Treasury, Fiscal Data portal, consumer complaints received by the

Bureau, and administrative data on borrowers in default provided by the

Department of Education. The report also leverages data and findings

from other reports, studies, and sources, and cites to these sources

accordingly. Readers should note that estimates drawn from survey data

are subject to measurement error resulting, among other things, from

reporting biases and question wording.

Survey of Income and Program Participation

The

Survey of Income and Program Participation (SIPP) is a nationally

representative survey of U.S. households conducted by the U.S. Census

Bureau. The SIPP collects data from about 20,000 households (40,000

people) per wave. The survey captures a wide range of characteristics

and information about these households and their members. The CFPB

relied on a pooled sample of responses from 2018, 2019, 2020, and 2021

waves for a total number of 17,607 responses from student loan borrowers

across all waves, including 920 respondents with student loans

receiving Social Security benefits. The CFPB’s analysis relied on the

public use data. To capture student loan debt, the survey asked to all

respondents (variable EOEDDEBT): Owed any money for student loans or

educational expenses in own name only during the reference period. To

capture receipt of Social Security benefits, the survey asked to all

respondents (variable ESSSANY): “Did … receive Social Security

benefits for himself/herself at any time during the reference period?”

To capture amount of Social Security benefits, the survey asked to all

respondents (variable TSSSAMT): “How much did … receive in Social

Security benefit payment in this month (1-12), prior to any deductions

for Medicare premiums?”

The

Federal Reserve Board’s Survey of Household Economics and

Decision-making (SHED) is an annual web-based survey of households. The

survey captures information about respondents’ financial situations. The

CFPB relied on a pooled sample of responses from 2019 through 2023

waves for a total number of 1,376 responses from student loan borrowers

in collection across all waves. The CFPB analysis relied on the public

use data. To capture default and collection, the survey asked all

respondents with student loans (variable SL6): “Are you behind on

payments or in collections for one or more of the student loans from

your own education?” To capture receipt of Social Security benefits, the

survey asked to all respondents (variable I0_c): “In the past 12

months, did you (and/or your spouse or partner) receive any income from

the following sources: Social Security (including old age and DI)?”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}