A new survey of federal student loan borrowers by the Institute for College Access and Success, a nonprofit focused on college affordability, found that about a fifth of borrowers are currently in either delinquency or default.

“These findings bring even greater urgency to ongoing concerns about a looming ‘default cliff,’ where an unprecedented number of borrowers struggle so much to repay their loans that they default on their payments in droves,” Michele Zampini, TICAS’s associate vice president for federal policy and advocacy, wrote in a blog post.

The Department of Education itself acknowledged a potential default cliff in an August data release, Zampini noted, writing that, although no new borrowers had defaulted since payments were paused in March 2020, many delinquent borrowers were in danger of defaulting after that pause ended.

Zampini also wrote that student loan default “comes with severe and punitive consequences.”

Just over half of respondents (52 percent) said their debt has negatively affected their ability to save for retirement, and 45 percent said the same about their ability to find and afford housing. Slightly fewer participants said that their student loan debt was “worth it”—41 percent—than said it wasn’t, at 48 percent. Advanced degree holders were more likely to consider their debt “worth it” than those with an associate or bachelor’s degree, as were male borrowers compared to female borrowers.

During National Transfer Student Week, I had the opportunity to present my dissertation findings. I was eager to share insights and connect with others doing similar work. Yet my excitement quickly gave way to disappointment: Multiple organizations were hosting overlapping events. Would anyone attend my session if there were other opportunities?

That moment clarified, for me, a larger truth about the transfer ecosystem. Despite our shared commitment to improving outcomes for transfer students, we often work in parallel rather than in partnership. True, sustained collaboration remains one of the missing links in creating a more coherent and equitable transfer experience.

Some Context

Collaboration should be the connective tissue of the transfer ecosystem. No single institution, system or organization can solve the challenges of transfer alone. When institutions, state agencies, employers and organizations work together, they have a better chance of building workable and successful pathways. The literature has increasingly suggested this point. Aspen et al.’s Tackling Transfer initiative implies that isolated campus reforms will not be entirely successful.

It emphasizes strengthening partnerships and using shared data and goals to make improvements. Similarly, both versions of the Transfer Playbook advocate success via intentional, ongoing partnerships.

Professional associations echo this message. For example, the American Association of Collegiate Registrars and Admissions Officers’ new conference, called The Assembly, is rooted in collaboration across sectors and institutions to solve transfer and mobility problems. This shift positions the association as a platform for collaboration, not just a publisher of best practices. Likewise, the National Association of Higher Education Systems is spearheading initiatives in the transfer and mobility space because it understands the need to have system-level collaboration.

These references send a clear message: Collaboration is an important strategy to improve the learner’s experience. This is a fundamental shift in our focus. When we center collaboration on the learner experience, rather than on the institution, it shifts the focus and the opportunities. Rather than designing projects around the interests of a single campus, foundation, or consulting contract, collaboration gives us the opportunity to ask, “What happens to the student through the educational journey that prevents successful transfer, and how do we solve that together?”

Challenges and Opportunities

As essential as it is, collaboration seems to be a challenge. To truly accomplish a collaborative network, institutions and agencies will need to look beyond their own boundaries. They need to be willing to pause their own goals to complement, support or provide an opportunity to another group. This has influential and financial implications, but it may end up being a better use of limited and shrinking dollars.

Changing the nature of how we collaborate could afford more opportunities and have a big impact. Collaboration can be complicated for organizations whose funding depends on producing value through exposure, engagement or consulting revenue. Partnerships may overshadow individual organizational accomplishments and lead to future financial growth.

For institutions, grant dollars for improving transfer are so highly competitive that they are sometimes impossible to obtain. More likely than not, funders are looking for the largest impact for their dollar, and that often translates into large-scale system- or statewide initiatives that will affect the most students or provide a large enough data set. That goal immediately eliminates small colleges from opportunities, further reducing the chance for improvement at the institutions that often need it the most.

On campuses, the need for collaboration is just as clear. Advocating for transfer is not the job of a single person with “transfer” in their title. It requires coordinated action across admissions, advising, faculty governance, financial aid, registrar, student life and employer partnerships. AACRAO’s task force on transfer and the award of credit, for instance, highlights the importance of cross-functional teams in redesigning policies and communication so students experience a coherent—not conflicting—set of messages about how their credits move.

Interestingly, the very reports we rely on for guidance point toward a different path. The Tackling Transfer work, for example, is grounded in multistate, cross-sector collaboration and explicitly calls for understanding the incentives and disincentives that shape institutional behavior around transfer. Lumina’s guidance on building local talent ecosystems emphasizes that durable change comes from coalitions willing to redesign systems together, not from one-off pilot projects.

What If We …

So, what might it look like to take collaboration seriously across the transfer ecosystem? Consider these collaborations:

Build shared agendas and calendars. National, regional and virtual events could be coordinated through a master calendar or hub so that transfer professionals aren’t forced to choose between overlapping webinars and conferences hosted by organizations that share the same goals.

Co-create tools and publications. Instead of each group producing its own tool kits and reports, organizations might collaborate on cross-branded resources that show how their frameworks align. Treat multiple opportunities as complements, not competitors.

Align state and regional efforts with institutional partnerships. The literature on national transfer reform emphasizes that systems and regions are critical units of change. State agencies, coordinating boards and foundations can use this insight to convene partnerships that bring institutions, employers and community organizations to the same table.

Elevate practitioners as collaborators, not just implementers. The most effective transfer-focused reports and research draw heavily on the expertise of people doing the day-to-day work of advising, curriculum design and transcript evaluation. Our collaborations should be built with, not just for, these practitioners.

Expand professional development and knowledge. Ideas could be to offer membership deals across organizations that support transfer students to engage more people in professional development opportunities amid decreasing budgets. Or, create a centralized repository or organization that can serve as a single source of information, rather than the plethora of sites, agencies, organizations and companies offering current professional development and resources.

These aren’t small shifts. They require seeing ourselves not as competitors in the transfer space, but as collaborators of its progress.

And So …

If we truly want to strengthen the ecosystem, we must build structures that make collaboration the default and not the exception. Many of the publications we rely on and reference already pointing us there. The question is whether we will follow their lead, not just in language but in practice. By working together, we can move beyond fragmented efforts toward a shared vision of mobility, equity and opportunity for every learner who dares to transfer.

The “Default Cliff” Has Arrived — Here’s What It Means for You

Millions of borrowers are inching toward what experts call a student loan default cliff. According to new reports from the Congressional Research Service and CNBC, more than 9 million borrowers are behind on payments — with 5.3 million already in default and another 4.3 million just a few missed payments away.

Sen. Elizabeth Warren called it an “economic disaster in the making,” urging the Department of Education to act fast. But for borrowers, the more immediate question is simpler: What happens if my loans default — and can I fix it?

The short answer: yes, you can fix it.

Even if your student loans are in default, there are proven ways to recover, repair your credit, and get back into good standing. Here’s what default really means, why it’s spiking in 2025, and what steps you can take right now to get out.

What It Means to Default on Your Student Loans

Defaulting on your student loans means you’ve gone long enough without making payments that your lender or the federal government officially labels your debt as seriously past due.

For federal student loans, that happens after 270 days (about nine months) of missed payments without deferment, forbearance, or an active repayment plan. Once you hit that mark, your entire balance becomes due immediately — a process called acceleration — and your loan is transferred from your servicer to the Department of Education’s Default Resolution Group or a collection agency.

For private student loans, the timeline is shorter — usually 90 to 180 days of nonpayment, depending on the lender. Private loans don’t qualify for federal relief programs like income-driven repayment or rehabilitation, and lenders can move quickly to collections or even lawsuits.

In short: default turns your loan problem into a legal problem — one that can trigger collections, wage garnishment, and serious credit damage if left unaddressed.

What Happens When You Default on a Student Loan

Defaulting on your student loans can hit hard and fast. Here’s what to expect if it happens:

Your entire balance becomes due immediately. You lose access to flexible repayment options.

You lose federal benefits. That includes deferment, forbearance, new aid eligibility, and access to forgiveness programs.

Collection actions begin. Wage garnishment, tax refund seizure, or withheld Social Security benefits are common.

Your credit score drops. Many borrowers see a hit of 60 to 170 points, making it harder to qualify for loans, credit cards, or housing.

Additional fees pile on. Collection costs and interest can quickly inflate your balance.

The damage lingers. Default stays on your credit report for up to seven years.

That’s the tough part — but the good news is, you can reverse it. Through rehabilitation or consolidation, most borrowers can bring their loans back to good standing and start rebuilding credit within months.

Why Millions of Borrowers Are Facing Default in 2025

After years of pandemic relief, millions of borrowers are falling behind again as student loan payments resume. Reports from the Congressional Research Service show more than 5 million borrowers already in default and another 4 million close behind — what economists now call the “student loan default cliff.”

The End of Post-Pandemic Relief and the “Default Cliff”

When the post-pandemic relief period ended in fall 2024, many borrowers who hadn’t made payments in years suddenly had to restart them. Some managed to catch up, but millions didn’t — either because they couldn’t afford the new bills or never received clear guidance from their servicers.

With delinquency reporting and wage garnishments now back in play, defaults are climbing fast. Economists warn that this wave could squeeze consumer spending and credit access, particularly for families already stretched thin.

Policy Shifts Under the Big Beautiful Bill

The One Big Beautiful Bill Act (OBBB), signed in July 2025, made repayment even tougher for many. The law tightened borrowing limits, replaced familiar repayment plans like SAVE and REPAYE with new ones (RAP and revised IBR), and reduced access to relief programs.

At the same time, staffing cuts at the DoE left over 1 million IDR applications pending — meaning many borrowers are still waiting for payment adjustments that could prevent default.

Why Borrowers Are Falling Behind

Beyond policy, everyday economics are making repayment harder than ever:

Rising costs: Inflation and high housing prices are squeezing budgets.

Administrative delays: Servicer confusion and IDR backlogs leave many unsure of their payment status.

Borrower fatigue: After years of pauses and shifting policies, some borrowers simply checked out.

Defaults spreading: Even high-credit borrowers are missing payments, often prioritizing essentials over student loans.

The bottom line: the system restarted before it was ready, and millions are paying the price. But while the headlines sound grim, default isn’t permanent — there are still clear, proven ways to fix it and start fresh.

How to Fix a Defaulted Student Loan

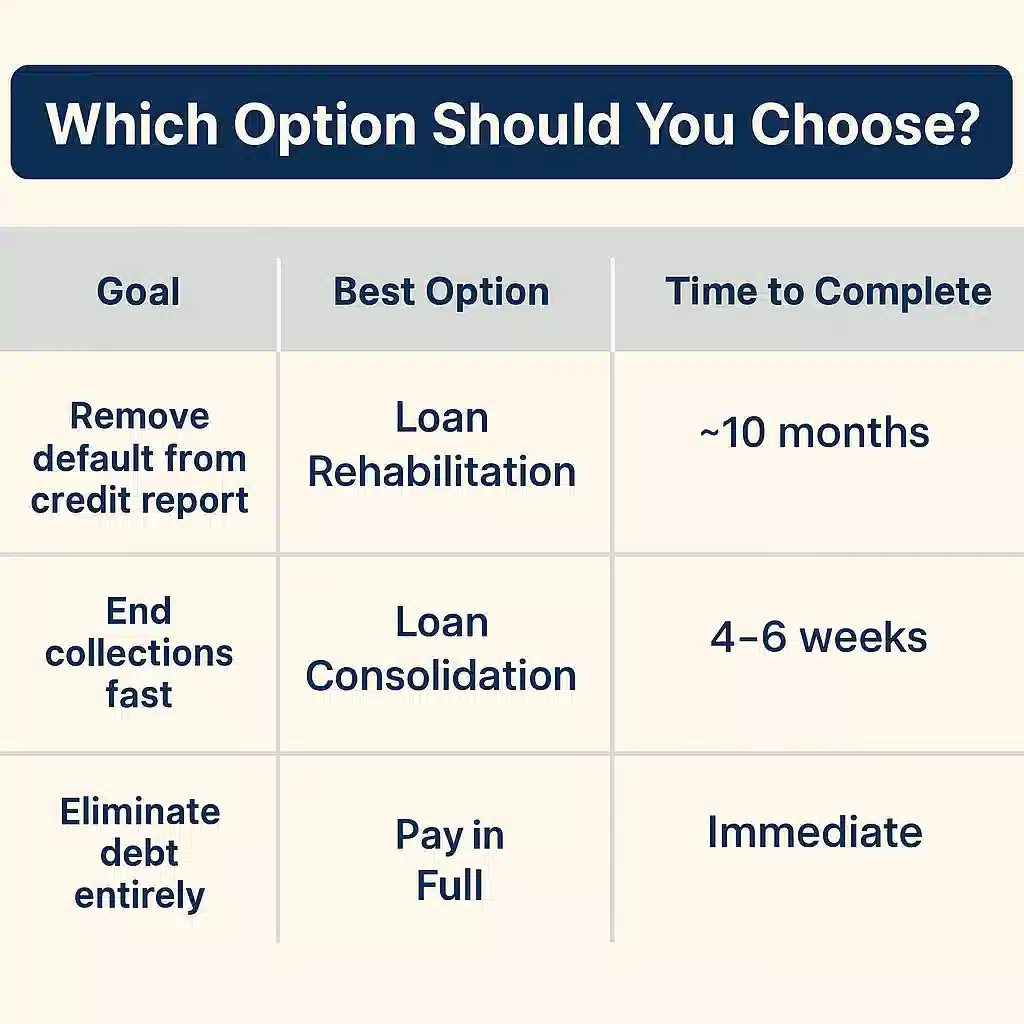

Default feels final, but it’s not. The federal system gives borrowers a few clear paths to recover, and most people can get back on track within months — not years.

The best way to fix student loan default depends on your situation, but for federal loans, there are three main options: rehabilitation, consolidation, and paying in full. (Private loans work differently — we’ll cover those next.)

Option 1: Loan Rehabilitation (Best for Credit Repair)

Loan rehabilitation is usually the best fix if you want to remove the default mark from your credit report and regain federal loan benefits.

You’ll make nine on-time monthly payments within ten months — typically around 15% of your discretionary income. If that’s too high, your servicer can set a lower amount (sometimes as little as $5) based on your financial situation.

Once you’ve made all nine payments:

Your loans are taken out of default and reassigned to a new servicer.

Collection actions like wage garnishment and tax refund seizures stop.

You regain eligibility for deferment, forbearance, forgiveness, and new aid.

The default is removed from your credit report (though late payments before default stay).

Best for: Borrowers who want to rebuild credit and have a steady enough income to make small monthly payments.

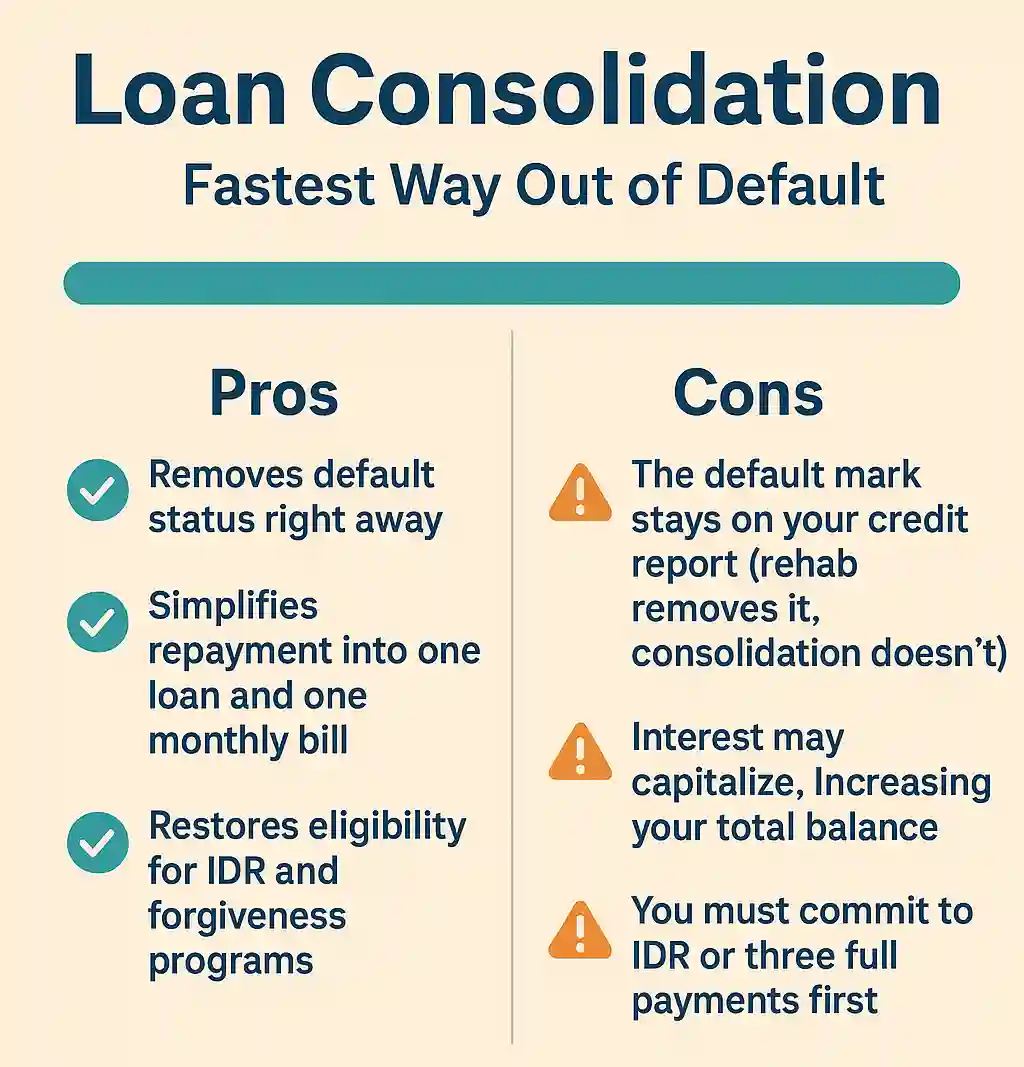

Option 2: Loan Consolidation (Fastest Way Out of Default)

If you need to get your loans out of default quickly, consolidation is faster. You’ll combine one or more defaulted federal loans into a new Direct Consolidation Loan, instantly bringing your account current.

To qualify, you must either:

Agree to repay the new loan under an income-driven repayment (IDR) plan, or

Make three consecutive, on-time, full monthly payments before consolidating.

Once approved, your new loan pays off the old ones, ending collections immediately.

Best for: Borrowers who need a fast fix or are facing wage garnishment or collection pressure.

Quick tip: If you plan to apply for a mortgage or new credit soon, consider rehabilitation first — it offers better long-term credit recovery, even if it takes longer.

Further Reading: Not sure whether rehabilitation or consolidation makes more sense for your situation? Check out our detailed comparison: Rehabilitation or Consolidation for Defaulted Student Loans? — it breaks down the pros, cons, fees, and long-term credit impact of each option.

Option 3: Paying the Loan in Full (Rare but Instant Fix)

If you can afford it, paying your defaulted loan in full is the quickest way to clear the debt and end all collection activity. Once paid, your loan is immediately considered current.

However, this isn’t realistic for most borrowers — and it doesn’t remove the default from your credit report. It simply stops the bleeding.

Best for: Borrowers with access to large funds (like an inheritance or settlement) who want to close the chapter on student debt entirely.

Once you’ve fixed the default, the next step is keeping it from happening again. The good news: that’s much easier — and it starts with setting up a repayment plan that actually fits your income.

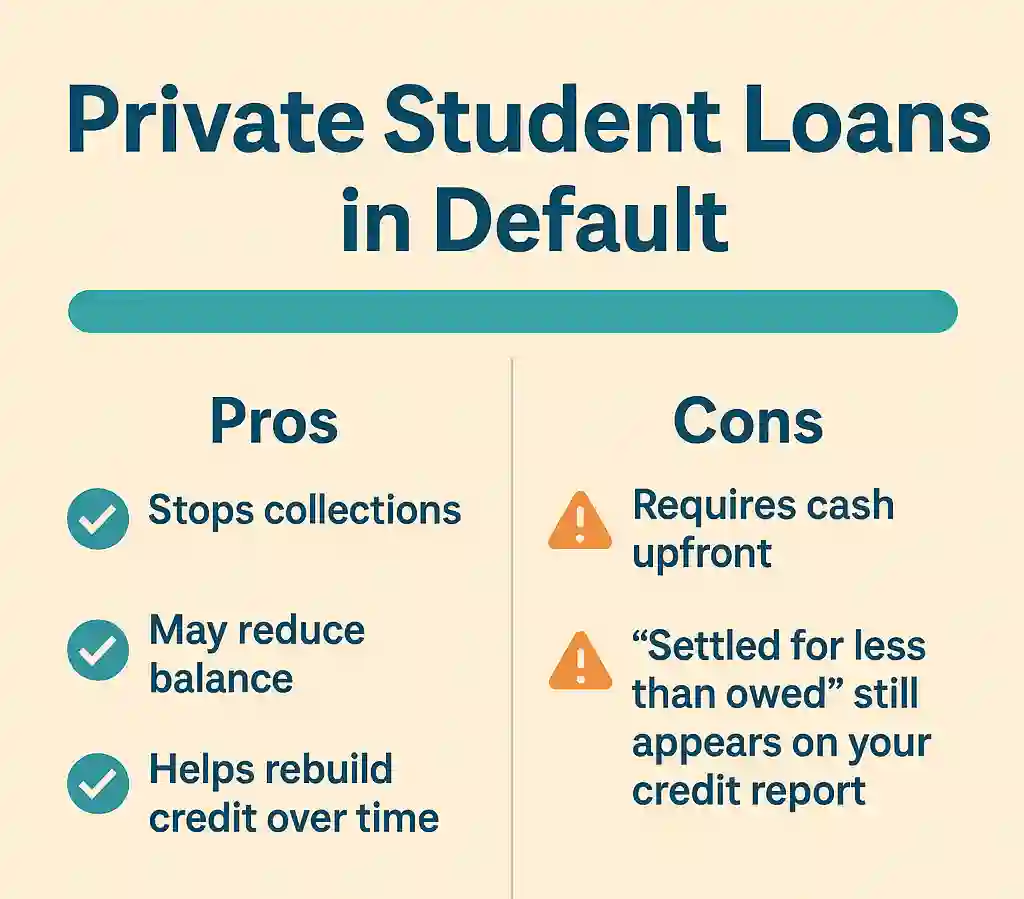

Private loans don’t follow federal rules, and they don’t offer rehabilitation. Most private lenders consider a loan in default after 90–180 days of missed payments.

If your private loan defaults:

Contact your lender immediately — many will negotiate new repayment terms to avoid litigation.

You can request a settlement, often paying 50–70% of the total balance in a lump sum or short-term plan.

Be aware that lawsuits are common. Private lenders can sue to garnish wages or seize assets (depending on state law).

Once you’ve fixed the default, the next step is keeping it from happening again. The good news: that’s much easier — and it starts with setting up a repayment plan that actually fits your income.

How to Avoid Student Loan Default Again

Once your loans are back in good standing, the goal is simple: keep them that way. The best way to avoid default again is to make your payments affordable, automatic, and always up to date — even when life gets messy.

Here’s how to stay out of the red for good:

1. Enroll in an Affordable Income-Driven Repayment Plan (IDR)

If your payments feel impossible, that’s a sign you’re probably on the wrong plan.

Switching to an IDR plan keeps monthly payments tied to your income and family size — not your loan balance.

As of 2025, the IBR plan and the new RAP are the most reliable options. The SAVE Plan is still in legal limbo, so new enrollments are limited, but IBR and RAP remain open and safe choices.

Enrolling in an IDR plan can:

Lower your payment to as little as $0 per month if your income qualifies.

Keep your account in good standing even if you’re earning very little.

Keep you eligible for forgiveness programs down the road.

If you’re unsure where to start, visit Studentaid.gov/idr and use the Loan Simulator to compare plans.

Related: Federal Student Loan Repayment Plan Options and Strategy — This article breaks down every repayment plan (SAVE, IBR, PAYE, and more) and explains how to pick the one that minimizes interest and maximizes forgiveness.

Pro tip: If your servicer hasn’t processed your IDR application yet, make at least one small monthly payment anyway — it helps prevent delinquency while you wait through the backlog.

2. Set Up Auto-Pay and Track Your Loan Status

It sounds obvious, but automation is the easiest way to prevent missed payments. Setting up auto-pay through your loan servicer ensures payments are made on time, every time — and you might even get a small interest rate discount (usually 0.25%).

Don’t just set it and forget it, though. Log in to your StudentAid.gov dashboard at least once a month to:

Check your payment history

Verify your servicer hasn’t changed (it happens more than you’d think)

Review your IDR recertification dates

Even a quick five-minute check can catch errors before they spiral into delinquency.

3. Recertify on Time (Even if the DOE Is Backlogged)

The Department of Education is still digging out from a massive 1.1 million IDR application backlog, which means your paperwork could sit for months. That’s why it’s critical to recertify early — ideally 60 to 90 days before your annual deadline.

If your income or family size changes, recertify right away to keep your payments accurate. Missing your recertification date can cause your payments to jump or your IDR plan to lapse, putting you back on a higher standard plan — the fastest path back to delinquency.

Bottom Line: Consistency Beats Perfection

Avoiding default isn’t about being perfect — it’s about staying consistent. Pick a repayment plan that fits your life, automate what you can, and keep tabs on your loans at least once a month.

Once you’ve climbed out of default, the hard part’s over. From here, it’s all about maintaining progress — and knowing where to get help before small problems turn into big ones.

Final Take

Defaulting on your student loans can feel like the end of the road — but it’s not. It’s a detour, not a dead end.

Millions of borrowers have been where you are right now and made it out. Whether you choose rehabilitation to clean up your credit or consolidation for a faster fix, the key is to take action before collections get worse. Once you’re out of default, enrolling in an affordable income-driven repayment plan and setting up auto-pay are your best defenses against sliding back.

If your loans are already in default, don’t ignore the problem — you can recover faster than you think. Check your status onStudentAid.gov, call your servicer, and start the process that fits your situation. Every payment, every step, moves you closer to financial stability and future forgiveness.

Ready to get back on track? Schedule a one-on-one consultation with Pedro Gomez, CFP®, and get a personalized plan to fix your default, choose the right repayment strategy, and rebuild your financial future — faster.

Federal student loans typically go into default after 270 days (about nine months) of missed payments without deferment, forbearance, or an active repayment plan. Private lenders often declare default sooner, usually after 90 to 180 days depending on the loan contract.

For federal loans, you can check your status on Studentaid.gov, which tracks your loan standing. For private loans, you need to monitor your loan servicer’s communications or check your credit report for defaults or collection entries.

The primary ways are loan rehabilitation, consolidation, or settlement. Rehabilitation requires nine on-time monthly payments and removes default status. Consolidation pays off the defaulted loan with a new loan, and settlement involves negotiating payoffs with lenders or collectors.

A federal student loan default typically stays on your credit report for seven years. However, successful rehabilitation removes the default status sooner, improving your credit profile more quickly.

Discharge of defaulted student loans is rare. It is usually granted only in cases of total and permanent disability, school closure, or very limited bankruptcy conditions. Regular discharge through bankruptcy is generally not allowed.

Pedro Gomez is the new Student Loan Sherpa and a Certified Financial Planner™ with over a decade of experience helping clients navigate complex financial decisions. He is the founder of Global Financial Plan, where he writes about international living, geoarbitrage, and strategies for retiring young, and also leads Brickell Financial Group, a registered investment advisory firm focused on accelerating financial freedom.

Pedro is the architect behind the “12 Levels of Financial Freedom” framework and blends student loan strategy with long-term planning, tax efficiency, and investing. His work is especially geared toward upwardly mobile professionals, entrepreneurs, and those looking to design a life beyond the default path.

Earlier this week the presidents of three of the formerly regional accreditors—Middle States, SACSCOC and WASC—hosted a webinar on AI and transfer credit. I watched, as did several colleagues; both topics are important, and since we’re covered by Middle States, it’s useful to know where its policies and expectations are heading. Credit loss upon transfer is a chronic issue on which accreditors have historically been muted; serious attention would be welcome.

It was … frustrating My colleagues and I tried afterward to isolate actual concrete changes and came away befuddled. It reminded me a bit of “strategic plans” that say things like, “We will achieve excellence.” OK, but that’s neither a strategy nor a plan. At best, it’s an intention.

Heather Perfetti, the president of MSCHE, stated that she doesn’t want accreditors to be seen as barriers to credit transfer; if anything, they’re urging a shift in the burden of proof for credit transfer from yes to no. That’s good, as far as it goes, but the key word is “urging.” Urging is not requiring. Kay McClenney famously noted that “students don’t do optional.” I’ve seen too many cases of universities not doing optional when it comes to accepting credits in transfer.

The stated reason is usually something about standards; the real reason is economic self-interest. Departments don’t want to “give away” any more credits than they have to, so they don’t. That changes only when orders come down from above—say, from a provost’s office because the college is desperate for enrollment, or from a State Legislature that got sick of shenanigans and passed a law, like MassTransfer in Massachusetts. Accreditors could conceivably play that role—it would be naïve to think that outcomes assessment would have gained the momentum it did without pressure from accreditors—but they’d have to put some force behind it. I didn’t catch any mention of that.

To be fair to the accreditors, that’s much harder now that they’ve lost their de facto regional monopolies. The regional accreditors are membership-driven organizations whose imprimatur opens up access to federal financial aid. Membership-driven organizations aren’t normally tough on their members, but the unusual combination of regional monopoly and access to federal financial aid gave them the leverage to push their members harder than they otherwise could. That didn’t always work out ideally—some colleges went bankrupt having recently satisfied accreditors that they were financially sound—but the structure made it at least possible for the accreditors to carry real weight.

The first Trump administration broke the regional monopolies and opened the door to alternative accreditors. Now there’s an entirely new body emerging in SACS’s territory, and colleges are empowered to shop around. When members can shop around for more lenient or ideologically aligned accreditors, it becomes more difficult for the legacy accreditors to issue mandates.

The new preference—I can’t call it a mandate or a policy—seems to mean that colleges should “default to yes” on credit transfer, in the absence of evidence that they shouldn’t. It wasn’t immediately clear what would constitute evidence that they shouldn’t. Lack of regional accreditation isn’t supposed to be dispositive in itself. Over time, a college could track success rates of students in Calc II who transferred in Calc I from College X, and if the rate were low enough, they could cite that. But that would require first allowing everything in for several years to build a track record; after that, the politics of saying no would be more complicated.

The connection to AI, as near as I could tell, was that it would allow colleges to assess transcripts and issue transfer decisions much more quickly at scale. That would actually help. As one of the presidents put it—I should have written it down, but alas—the current system works like trading in a car for a new one but not being told the value of your trade-in until you’ve had the new one for a few months. It’s not consumer-friendly at all. If transfer credit decisions could be issued at the same time as admission and financial aid decisions, students would be much more able to make informed decisions. I have concerns about AI hallucinations in this context (and many others), but if defaulting to yes is built in, it might work at least as well as the current system.

So, I’ll give this shift a cheer and a half out of three. The direction is positive; I just hope they can find a way to move from an intention to a plan.