Amid continued growing global uncertainty, the First Minister has announced Scotland’s Programme for Government for 2025/26, its last before the Scottish election in May next year.

Amongst its many promises is a commitment to “work with partners to secure a long-term and sustainable future for further and higher education”.

Does that mean we can draw a collective sigh of relief? Well, not quite. Despite Scotland’s universities continuing to face an uncertain future, there’s little in the government’s plan for the next twelve months which is likely to give the higher (or wider tertiary) education sector much comfort.

In March, the Carnegie Trust for the Universities of Scotland published our first research report, marking the beginning of a new direction for the charity as we seek to increase our impact and voice on issues of equity and inclusion in higher education in Scotland.

The report by Ipsos highlighted public views on the value, accessibility and funding of universities. The study, the first of its kind in many years, was featured widely in the Scottish media, and appeared on the front pages of the Scotsman, the Herald and the Daily Telegraph.

Most newspapers led with the headline figure that 48 per cent of respondents to Ipsos’ poll would support a change to Scotland’s university tuition fee model based on ability to pay.

However, other than on Wonkhe, what wasn’t picked up by many was what the polling tells us about the varied ways in which age, geography and wealth appear to have shaped how Scottish people have experienced and benefitted from the current post-school system.

Understanding the public’s views

The Trust’s interest in commissioning the research was to fill a hole in the evidence base – the public voice having been all but absent from recent discussions around the future of post-school education and skills in Scotland. Whether we or our politicians agree with the public is not really the point. Instead, we have a duty to ask why those views exist and what they might mean for the future of the system.

Alongside the 48 per cent who would support a change in the tuition fee model, a similar figure (49 per cent) expressed the view that studying courses that don’t directly lead to a profession is a waste of time. There are many ways in which higher education brings value to the individual and society underpinned by evidence, but clearly something in that messaging is falling short.

As a Trust that has always championed funding across the full curriculum, and as someone whose own undergraduate degree did not point to obvious employment, that is a challenging outlook. However, it’s important to acknowledge this opinion and to reflect on the reasons why nearly half the Scottish public feels this way.

In highlighting some of the nuance within public attitudes, we had hoped that the debate on funding might be able to move forwards from its current stasis – that the ground might be laid or a more open, grown-up and intelligent discussion on how we might address some of the challenges in the current system.

Unfortunately, the immediate reaction from the government wasn’t to acknowledge the public’s opinions, but to double down on the current policy.

I suppose, on reflection, this shouldn’t be surprising. Free tuition is a hallmark of Scottish devolution and a promise of what a modern Scotland would offer its people; part of a “social contract” between the government and its citizens.

To question it would be to question the social and democratic principles which underpin it and, it follows, that stepping away from it, even showing a willingness to entertain alternatives, would be to betray those values. It would certainly involve admission and acceptance that, despite its aspirations, the policy does not necessarily reflect the reality of the structures in which it is implemented.

But the reality is that free tuition sits in a wider operating context. The policy might be uniquely Scottish (at least in the UK), but as we have seen, the external factors that impact on it, are not within the current government’s direct control.

Our report was published just days after the latest statistics showed a sharp drop in international students attending university in Scotland, and in the same week as the UK Chancellor’s Spring Statement which the IFS estimated will cut the Scottish Budget by £400m by 2030.

It also came days before the Scottish Government announced that it had failed to deliver its interim child poverty targets, despite significant additional investment in social security. Continuing to operate the current higher education funding policy, already under strain, against this backdrop looks set to become considerably more challenging in coming years.

What should the priorities be for post-school education funding?

Delivering “free tuition” in the current context already means drawing lines in the sand. Currently these are drawn around full-time education (those studying part-time are means-tested and can’t currently access maintenance loans), the number of years of public support (for most people the length of the course plus one – the Trust picks up the tab for many students whose learner journeys are atypical), and around the number of places available to Scottish students (controversially capped according to the available budget and, as such, allegedly more competitive than rUK and international places).

They are also drawn around undergraduate courses (there are no government grants available for students to access postgraduate study) and university funding itself, despite the implications for colleges and apprenticeships which come from the same portfolio budget. It’s these choices – and they are choices – which determine who benefits from post-school education funding and have led some people to claim the current system is not only unaffordable, but unfair.

In defending the government’s policy, the Minister was unequivocal that “our support for free tuition is about more than ideology – it was founded on an equity-of-access approach [and] is based on simple logic”.

This deserves some unpicking because there is a clear difference between a universal approach based on equality, where everyone gets the same, and equity, where resources are directed to those who need them the most in order to deliver equal outcomes.

In a system of finite and diminishing resources, the former approach can simply serve to further embed inequalities as those with capital (be that economic or social) are better able to navigate the system, making them more likely to reap the rewards. Put simply, it’s not so easy to draw a direct line between free tuition and fair access.

A more equitable approach?

When Andrew Carnegie set up the Carnegie Trust for the Universities of Scotland, it was equity that was the driving force. His treatise on philanthropy, The Gospel of Wealth sets out that he saw it as the responsibility of those who were fortunate enough to be rich, to use their surplus wealth in a manner which would benefit society.

Carnegie sought to instill this ideology within the Trust, to ensure that ‘no capable student should be de-barred from attending the university on account of the payment of fees.’ However, he was clear about who should benefit, noting that the honest pride for which my countrymen are distinguished would prevent applications from those who didn’t need the Trust’s assistance.

He went further and built this benevolence into the Trust’s governance as it became the only one of his Trusts to date that could accept donations to:

…enable such students as prefer to do so to consider the payments made on their account merely as advances which they resolve to repay if ever in a position to do so….

In the first half of the 20th century this approach was instrumental in expanding access to higher education to enable individuals from disadvantaged backgrounds, including record numbers of women, to benefit from its rewards.

By 1910 the Trust was responsible for funding around half of the students going to university in Scotland. To put that in today’s terms, that’s 50 per cent of students in Scotland from “widening access” backgrounds.

Compare that to the current day. On paper Scotland has made impressive progress on widening access in the last ten years. Recent statistics show 16.7 per cent of Scottish first-degree entrants in 2023/24 were from the poorest neighborhoods.

But as many have highlighted the current national indicator for widening access, SIMD20, is not a measure of household or individual deprivation, and therefore masks a complex landscape of inequality. In other words, in spite of nearly two decades of free tuition, inequalities exist and persist. Data on graduate outcomes suggests that those from wealthier backgrounds are more likely to complete their degrees and to benefit most in the labour market, and we can see from the Ipsos survey that those from high earning households are also less likely to support changes to funding in which they or their families aren’t direct beneficiaries.

Is university still worth it?

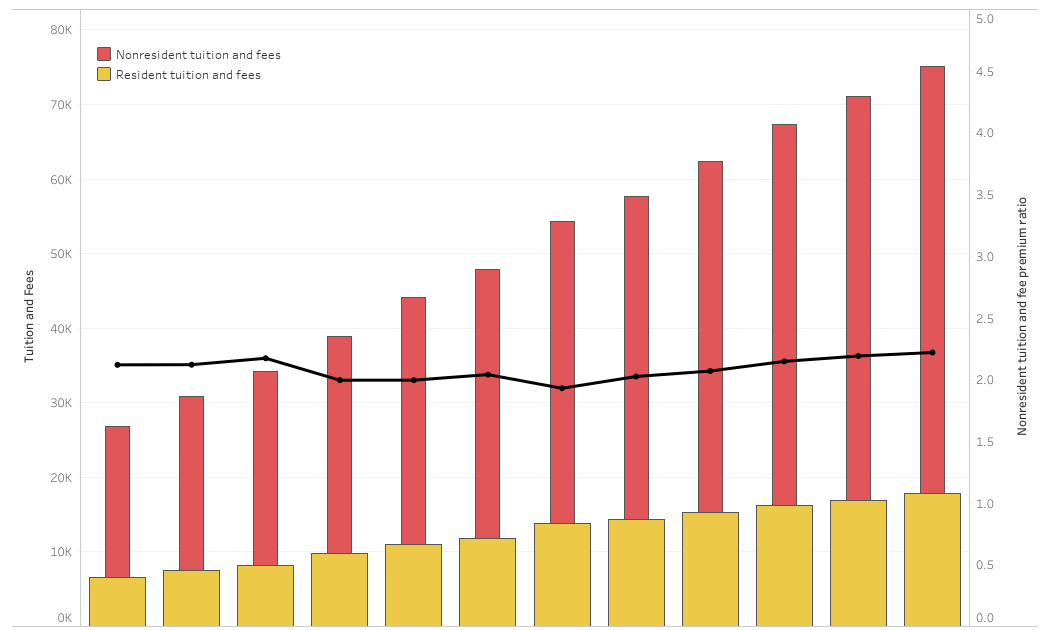

To demonstrate the success of free tuition, the government has pointed to the record numbers of students from Scotland securing places at university. But the rewards for those students are also changing. The IFS has noted a worrying downward trend in the graduate premium (the amount a graduate can expect to earn compared to a non-graduate) which has fallen by at least 10 per cent in the period 1997 to 2019.

This perhaps explains why the Ipsos polling shows that the public are less certain about the value of attending university nowadays. The IFS also note issues of underemployment of graduates. In 2021/22, around a quarter of graduates who participated in the HESA graduate outcomes survey weren’t in graduate jobs and if we dive into access to postgraduate qualifications, where it’s suggested the wage premium jumps by around 20-40 per cent, we would be forgiven for questioning whether inequality has simply shifted further up the pipe.

It is in this light that the Scottish Government response disappoints. Rather than showing desire to understand the views of their constituents, or to explore the evidence, we just keep returning to the same unqualified maxim, that access to higher education should be based on “ability to learn” rather than “ability to pay”.

A more intelligent response would surely be to acknowledge the ideals and aspirations underpinning free tuition and engage in an exploration of whether those are being met through the current approach and, if not, how best to deliver them in the current context.

Were that to happen we might instead be able to have a discussion, not about the concept of free tuition, but about whether it is possible to identify a funding approach that is at once “free”, “equitable” and “sustainable” and about where we might draw lines around public investment in tertiary education in a way that will best deliver on Scotland’s outcomes and ambitions.

Injecting some democracy into the funding debate

Central to the success of such a debate should also be a commitment to engage with the public on what they want from the post school system and how we can deliver that in today’s Scotland.

Our sister organization, Carnegie UK’s Life in the UK 2024 index for Scotland shows that public trust in government and politics has reached a record low with nearly two thirds of people feeling that they have no influence over decisions affecting the country. That’s likely in no small part due to the gap between policy promises and the ways in which they find expression in Scotland’s communities. In this context, continuing to stick to a now decades-old policy position without attempting to evaluate it appears, at best, short-sighted and, at worst, undemocratic.

To address this there are calls for more participative forms of engagement which have been shown to provide opportunities for diverse groups to be involved in decision-making; shaping and enhancing policy development to deliver improved outcomes that meet a wider range of needs. The Citizen Jury we’ll be running with Ipsos this year intends to do just that.

It will bring together a diverse group of people from across Scotland to consider evidence on tertiary education funding and make recommendations for the future. This could be an opportunity to rebuild public trust and to develop a new social contract, one that is co-produced with citizens. Our political leaders in Scotland should care about that and not be too quick to dismiss the public attitudes we’re working to uncover.