[Editor’s note: Please let us know of any corrections, additions, or broken links. We always welcome your feedback.]

This list traces how U.S. higher education has been reshaped by neoliberal policies, privatization, and data-driven management, producing deepening inequalities across race and class. The works examine the rise of academic capitalism, growing student debt, corporatization, and the influence of private interests—from for-profit colleges to rankings and surveillance systems. Together, they depict a sector drifting away from its public mission and democratic ideals, while highlighting the structural forces that created today’s crises and the reforms needed to reverse them.

Ahn, Ilsup (2023). The Ethics of Educational Healthcare: Student Debt, Neoliberalism, and Justice. Palgrave Macmillan.

Alexander, Bryan (2020). Academia Next: The Futures of Higher Education. Johns Hopkins Press.

Alexander, Bryan (2023). Universities on Fire. Johns Hopkins Press.

Alexander, Bryan (2026). Peak Higher Ed. Johns Hopkins Press.

Angulo, A. (2016). Diploma Mills: How For-profit Colleges Stiffed Students, Taxpayers, and the American Dream. Johns Hopkins University Press.

Apthekar, Bettina (1966). Big Business and the American University. New Outlook Publishers.

Apthekar, Bettina (1969). Higher Education and the Student Rebellion in the United States, 1960–1969: A Bibliography.

Archibald, R. & Feldman, D. (2017). The Road Ahead for America’s Colleges & Universities. Oxford University Press.

Armstrong, E. & Hamilton, L. (2015). Paying for the Party: How College Maintains Inequality. Harvard University Press.

Arum, R. & Roksa, J. (2011). Academically Adrift: Limited Learning on College Campuses. University of Chicago Press.

Baldwin, Davarian (2021). In the Shadow of the Ivory Tower: How Universities Are Plundering Our Cities. Bold Type Books.

Barr, Andrew & Turner, Sarah (2023). The Labor Market Returns to Higher Education. Oxford University Press.

Bennett, W. & Wilezol, D. (2013). Is College Worth It? Thomas Nelson.

Berg, I. (1970). The Great Training Robbery: Education and Jobs. Praeger.

Berman, Elizabeth P. (2012). Creating the Market University. Princeton University Press.

Berman, Elizabeth Popp & Stevens, Mitchell (eds.) (2019). The University Under Pressure. Emerald Publishing.

Berry, J. (2005). Reclaiming the Ivory Tower: Organizing Adjuncts to Change Higher Education. Monthly Review Press.

Berry, J. and Worthen, H. (2021). Power Despite Precarity: Strategies for the Contingent Faculty Movement in Higher Education. Pluto Books.

Best, J. & Best, E. (2014). The Student Loan Mess. Atkinson Family Foundation.

Bledstein, Burton J. (1976). The Culture of Professionalism. Norton.

Bogue, E. Grady & Aper, Jeffrey (2000). Exploring the Heritage of American Higher Education.

Bok, D. (2003). Universities in the Marketplace. Princeton University Press.

Bousquet, M. (2008). How the University Works. NYU Press.

Brennan, J. & Magness, P. (2019). Cracks in the Ivory Tower. Oxford University Press.

Brint, S. & Karabel, J. (1989). The Diverted Dream. Oxford University Press.

Burawoy, Michael & Mitchell, Katharyne (eds.) (2020). The University, Neoliberalism, and the Politics of Inequality. Routledge.

Burd, Stephen (2024). Lifting the Veil on Enrollment Management: How a Powerful Industry is Limiting Social Mobility in American Higher Education. Harvard Education Press

Cabrera, Nolan L. (2018). White Guys on Campus. Rutgers University Press.

Cabrera, Nolan L. (2024). Whiteness in the Ivory Tower. Teachers College Press.

Cantwell, Brendan & Robertson, Susan (eds.) (2021). Research Handbook on the Politics of Higher Education. Edward Elgar.

Caplan, B. (2018). The Case Against Education. Princeton University Press.

Cappelli, P. (2015). Will College Pay Off? Public Affairs.

Carney, Cary Michael (1999). Native American Higher Education in the United States. Transaction.

Cassuto, Leonard (2015). The Graduate School Mess. Harvard University Press.

Caterine, Christopher (2020). Leaving Academia. Princeton Press.

Childress, H. (2019). The Adjunct Underclass. University of Chicago Press.

Chomsky, Noam (2014). Masters of Mankind. Haymarket Books.

Choudaha, Rahul & de Wit, Hans (eds.) (2019). International Student Recruitment and Mobility. Routledge.

Cohen, Arthur M. (1998). The Shaping of American Higher Education. Jossey-Bass.

Collins, Randall (1979/2019). The Credential Society. Columbia University Press.

Cottom, Tressie McMillan (2016). Lower Ed.

Cottom, Tressie McMillan & Darity, William A. Jr. (eds.) (2018). For-Profit Universities. Routledge.

Domhoff, G. William (2021). Who Rules America? Routledge.

Donoghue, F. (2008). The Last Professors.

Dorn, Charles (2017). For the Common Good. Cornell University Press.

Eaton, Charlie (2022). Bankers in the Ivory Tower. University of Chicago Press.

Eisenmann, Linda (2006). Higher Education for Women in Postwar America. Johns Hopkins Press.

Espenshade, T. & Walton Radford, A. (2009). No Longer Separate, Not Yet Equal. Princeton University Press.

Faragher, John Mack & Howe, Florence (eds.) (1988). Women and Higher Education in American History. Norton.

Farber, Jerry (1972). The University of Tomorrowland. Pocket Books.

Freeman, Richard B. (1976). The Overeducated American. Academic Press.

Gaston, P. (2014). Higher Education Accreditation. Stylus.

Gildersleeve, Ryan Evely & Tierney, William (2017). The Contemporary Landscape of Higher Education. Routledge.

Ginsberg, B. (2013). The Fall of the Faculty. Oxford University Press.

Giroux, Henry (1983). Theory and Resistance in Education. Bergin and Garvey Press.

Giroux, Henry (2014). Neoliberalism’s War on Higher Education. Haymarket Books.

Giroux, Henry (2022). Pedagogy of Resistance. Bloomsbury Academic.

Gleason, Philip (1995). Contending with Modernity. Oxford University Press.

Golden, D. (2006). The Price of Admission.

Goldrick-Rab, S. (2016). Paying the Price.

Graeber, David (2018). Bullshit Jobs. Simon and Schuster.

Groeger, Cristina Viviana (2021). The Education Trap. Harvard Press.

Hamilton, Laura T. & Kelly Nielson (2021). Broke.

Hampel, Robert L. (2017). Fast and Curious. Rowman & Littlefield.

Hirschman, Daniel & Berman, Elizabeth Popp (eds.) (2021). The Sociology of Higher Education.

Johnson, B. et al. (2003). Steal This University.

Kamenetz, Anya (2006). Generation Debt. Riverhead.

Keats, John (1965). The Sheepskin Psychosis. Lippincott.

Kelchen, Robert (2018). Higher Education Accountability. Johns Hopkins University Press.

Kezar, A., DePaola, T., & Scott, D. (2019). The Gig Academy. Johns Hopkins Press.

Kinser, K. (2006). From Main Street to Wall Street.

Kozol, Jonathan (1992). Savage Inequalities. Harper Perennial.

Kozol, Jonathan (2006). The Shame of the Nation. Crown.

Kraus, Neil (2023). The Fantasy Economy: Neoliberalism, Inequality, and the Education Reform Movement. Temple University Press, 2023.

Labaree, David (1997). How to Succeed in School Without Really Learning. Yale University Press.

Labaree, David F. (2017). A Perfect Mess. University of Chicago Press.

Lafer, Gordon (2004). The Job Training Charade. Cornell University Press.

Loehen, James (1995). Lies My Teacher Told Me. The New Press.

Lohse, Andrew (2014). Confessions of an Ivy League Frat Boy. Thomas Dunne Books.

Lucas, C.J. (1994). American Higher Education: A History.

Lukianoff, Greg & Haidt, Jonathan (2018). The Coddling of the American Mind. Penguin Press.

Maire, Quentin (2021). Credential Market. Springer.

Mandery, Evan (2022). Poison Ivy. New Press.

Marginson, Simon (2016). The Dream Is Over. University of California Press.

Marti, Eduardo (2016). America’s Broken Promise. Excelsior College Press.

Mettler, Suzanne (2014). Degrees of Inequality. Basic Books.

Morris, Dan & Targ, Harry (2023). From Upton Sinclair’s ‘Goose Step’ to the Neoliberal University.

Newfeld, C. (2011). Unmaking the Public University.

Newfeld, C. (2016). The Great Mistake.

Newfield, Christopher (2023). Metrics-Driven. Johns Hopkins Press.

O’Neil, Cathy (2016). Weapons of Math Destruction. Crown.

Palfrey, John (2020). Safe Spaces, Brave Spaces. MIT Press.

Paulsen, M. & Smart, J.C. (2001). The Finance of Higher Education. Agathon Press.

Piketty, Thomas (2020). Capital and Ideology. Harvard University Press.

Reynolds, G. (2012). The Higher Education Bubble. Encounter Books.

Rojstaczer, Stuart (1999). Gone for Good. Oxford University Press.

Rosen, A.S. (2011). Change.edu. Kaplan Publishing.

Roth, G. (2019). The Educated Underclass. Pluto Press.

Ruben, Julie (1996). The Making of the Modern University. University of Chicago Press.

Rudolph, F. (1991). The American College and University.

Rushdoony, R. (1972). The Messianic Character of American Education. The Craig Press.

Schrecker, Ellen (2010). The Lost Soul of Higher Education: New Press.

Selingo, J. (2013). College Unbound.

Shelton, Jon (2023). The Education Myth. Cornell University Press.

Simpson, Christopher (1999). Universities and Empire. New Press.

Sinclair, U. (1923). The Goose-Step.

Slaughter, Sheila & Rhoades, Gary (2004). Academic Capitalism and the New Economy. Johns Hopkins University Press.

Smyth, John (2017). The Toxic University. Palgrave Macmillan.

Sperber, Murray (2000). Beer and Circus. Holt.

Stein, Sharon (2022). Unsettling the University. Johns Hopkins Press.

Stevens, Mitchell L. (2009). Creating a Class. Harvard University Press.

Stodghill, R. (2015). Where Everybody Looks Like Me.

Tamanaha, B. (2012). Failing Law Schools. University of Chicago Press.

Tatum, Beverly (1997). Why Are All the Black Kids Sitting Together in the Cafeteria? Basic Books.

Taylor, Barret J. & Cantwell, Brendan (2019). Unequal Higher Education. Rutgers University Press.

Thelin, John R. (2019). A History of American Higher Education. Johns Hopkins Press.

Tolley, K. (2018). Professors in the Gig Economy. Johns Hopkins University Press.

Trow, Martin (1973). Problems in the Transition from Elite to Mass Higher Education. Carnegie Commission on Higher Education.

Twitchell, James B. (2005). Branded Nation. Simon and Schuster.

Vedder, R. (2004). Going Broke By Degree.

Veysey, Lawrence R. (1965). The Emergence of the American University.

Washburn, J. (2006). University Inc.

Washington, Harriet A. (2008). Medical Apartheid. Anchor.

Whitman, David (2021). The Profits of Failure. Cypress House.

Wilder, C.D. (2013). Ebony and Ivy.

Winks, Robin (1996). Cloak and Gown. Yale University Press.

Woodson, Carter D. (1933). The Mis-Education of the Negro.

Zaloom, Caitlin (2019). Indebted. Princeton University Press.

Zemsky, Robert, Shaman, Susan & Baldridge, Susan Campbell (2020). The College Stress Test. Johns Hopkins University Press.

Zuboff, Shoshana (2019). The Age of Surveillance Capitalism. PublicAffairs.

Activists, Coalitions, Innovators, and Alternative Voices

College Choice and Career Planning Tools

Innovation and Reform

Higher Education Policy

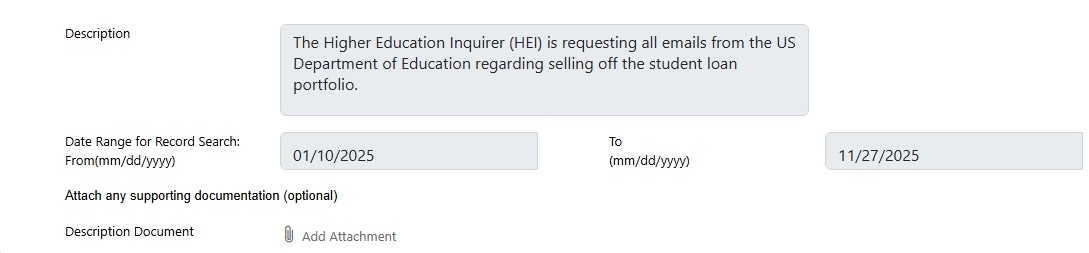

Data Sources

Trade publications

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}