If you applied for a private student loan and were notified that you need to apply with a cosigner, you’re not alone. Over 90% of private student loans include a cosigner, which is an individual — usually a parent or guardian — who is willing to take equal responsibility for the loan alongside you, the primary borrower.

Why do I need a cosigner?

To assess your ability to repay your student loan, private lenders typically require a credit and income check. Given that most student loan borrowers are fresh out of high school or in their early twenties, many do not have sufficient credit history, or if they do, their credit score is low.

Credit history is built over time through credit cards, mortgages, car loans, etc., and many students have not yet encountered these responsibilities. As a result, student borrowers are often prompted to apply with a cosigner, who has an established income and a history of repaying debts on time.

Who can be a cosigner?

When considering who can cosign your loan, the most important trait is reliability and good credit. This will not only help you secure your loan, but possibly lower your interest rate, as well.

A lower interest rate can make a big difference in the amount of money you’ll owe, overall.

How can I find a cosigner?

When thinking about how to find a cosigner, consider this question: “Who do I know will be sitting at my graduation, cheering me on as I walk across the stage to receive my diploma?”

By starting here, you will identify individuals who are invested in your success and achievement. Parents and guardians are a great place to start. Aunts, uncles, grandparents, or older siblings can also be good options.

Once you identify the person who can be a cosigner, gather and organize all of the information about the loan in preparation for any questions your cosigner might have.

Here are a few they might ask:

Why are you applying for this loan?

How much are you applying for?

Who is the lender?

Why do you need a cosigner?

When approaching someone to cosign your loan, be sure to communicate that you intend to be trustworthy and repay your loan on time. Your cosigner is equally responsible for your loan, so any missed payments by you will also negatively affect their credit history.

If they ask why you’re applying for this loan, it would be a good idea to show them your school of choice, the cost of attendance, and any other financial aid you’ve already received, and the remaining balance you need the loan to cover. This will keep your cosigner informed and will help them understand why the loan is necessary. Opening up about your finances to a person you trust could be helpful — they may be able to offer advice on how to best navigate repaying the loan and life beyond college.

At College Ave, we can provide you with an email that you can send directly to your cosigner. This email contains useful information about applying for a student loan as a cosigner, but we recommend first having an in-person discussion with the individual you plan to ask.

Why Undergraduates and Graduates May Need Cosigners

Private lenders, like College Ave, rely on credit scores, proof of income, repayment history, and other factors to determine whether a borrower is eligible for a loan and will be able to repay it.

Undergraduate students usually have little to no credit history and limited income. This makes it hard for a lender to assess if they’ll be able to repay their loan on their own. A cosigner can improve odds of getting an application approved, secure a lower interest rate, and more favorable terms. Cosigning a loan also enables the undergrad to establish and build their credit history.

Graduate students may also need or want a cosigner to secure a private student loan for the same reasons listed above — improved approval odds, favorable rates and terms, etc. Though graduate students are older, they may still have limited credit and/or high existing debt from undergrad loans or other living expenses.

Remember, you might need a cosigner for other things too—like renting an apartment. That same person could be a great option to help cosign your undergraduate or graduate private student loan.

How do I know if my cosigner will qualify?

At College Ave, we offer a credit pre-qualification tool that will tell you if your credit qualifies for a loan and what interest rates you can expect. This can be filled out prior to applying. After asking your cosigner, it is a good idea to have that individual use the pre-qualification tool, too, to see if their credit qualifies.

Negotiations were held in-person for one week at the beginning of October and a second week in November.

Pete Kiehart/The Washington Post/Getty Images

A very limited number of degree programs would have access to the highest level of loans under a new set of regulations that the Department of Education and its negotiating committee signed off on Thursday.

The regulations, written in response to the loan caps of Congress’s One Big Beautiful Bill Act, allow students in programs that qualify as professional to take out up to $200,000. Meanwhile, graduate students will only be able to take out up to $100,000.

What was up for debatethroughout the two-week negotiation process was which degree programs qualify for which level of loans.

And while Thursday’s definition of professional programs was slightly more inclusive than the department’s original suggestion—a list of 10 degrees, including medicine, law, dentistry and a masters of divinity—they are not as expansive as a third proposal put forward by Alex Holt, the committee member representing taxpayers and public interest.

The final definition limits professional programs to the original 10 programs, a doctorate in clinical psychology, and a handful of other doctorate programs that fall within the same four-digit CIP codes. By comparison, Holt’s plan would have included any program that is 80 credit hours long, regardless of whether it was a master’s or doctorate degree, so long as it fell within the same two-digit CIP code. (A CIP code, otherwise known as the Classification of Instructional Programs, is part of an organizational system used by ED to group similar academic programs.)

On Thursday, before the committee’s final consensus vote, department officials explained to committee members that if they did not agree to their definition of a professional degree, they could lose out on other “concessions” they had won from the department. Without consensus, the department would legally be free to rewrite any aspect of the proposal prior to releasing it for public comment. (The proposal that reached consensus will still be subject to public comment.)

“I also would like to remind everyone of numerous things that we have chosen to do in these negotiations that you requested for us to do,” said Tamy Abernathy, the department’s negotiator, before listing a slew of other changes the department made concerning the transition to new loan repayment plans and how to grandfather in existing borrowers to new loan policies.

Under Secretary Nicolas Kent noted before the vote that the proposal was “not a perfect definition, but … a perfect definition for the purposes of consensus.”

“We recognize that not every stakeholder group will be thrilled about our proposal,” Kent said. “But I want to remind everybody what consensus means, and that means that if you all agree, or can live with it—because we don’t have to love it—that we will take that regulatory language and put it into the notice of proposal.”

Multiple committee members told Inside Higher Ed they agreed with Kent’s evaluation of what it took to reach a compromise.

Kent closed the meeting by noting that “because we’ve reached consensus, negotiators and their employers will refrain from commenting negatively … as they agreed to do.”

File photoThe Department of Education announced a new rule that would allow the agency to exclude certain nonprofit and government employers from the Public Service Loan Forgiveness program, targeting organizations that “engage in specific enumerated illegal activities” or do not align with the current administration’s priorities.

The rule, which was published Friday in the Federal Register, grants Education Secretary Linda McMahon unilateral authority to determine which organizations are ineligible for the program. It takes effect July 1, 2026.

According to critics, the rule could disqualify employees of sanctuary jurisdictions and nonprofit organizations that provide immigrant family support, gender-affirming care, diversity and equity programs, or assistance to protesters exercising First Amendment rights.

The Public Service Loan Forgiveness program was established by Congress in 2007 on a bipartisan basis. Under the program, federal, state, local and tribal government employees, as well as workers for 501(c)(3) nonprofit organizations, can have their remaining federal student loan debt forgiven after making 10 years of qualifying payments while working in public service. More than one million workers have received loan forgiveness through the program to date.

Two advocacy organizations, Democracy Forward and Protect Borrowers, issued a joint statement committing to challenge the rule in federal court.

“This is a direct and unlawful attack on nurses, teachers, first responders, and public service workers across the country,” the organizations said. “This new rule is a craven attempt to usurp the legislature’s authority in an unconstitutional power grab aimed at punishing people with political views different than the administration’s.”

Alexander Lundrigan, Higher Education Policy and Advocacy Manager at Young Invincibles, called the changes “illegal” and “politically motivated.”

“The administration cannot unilaterally rewrite a program that was passed into law by Congress,” Lundrigan said. “PSLF eligibility is defined by law, not political ideology.”

Jaylon Herbin, director of federal policy at the Center for Responsible Lending, agrees, adding that the regulation “is the latest in a long list of cruel tricks imposed on workers and groups who hold views or serve people this administration doesn’t like.”

He added that the restrictions “will consign millions of student borrowers to decades of unaffordable debt repayment and will worsen existing shortages of teachers, police and emergency services workers, and nonprofits who help local residents thrive and contribute to building vibrant, economically resilient communities.”

The “Default Cliff” Has Arrived — Here’s What It Means for You

Millions of borrowers are inching toward what experts call a student loan default cliff. According to new reports from the Congressional Research Service and CNBC, more than 9 million borrowers are behind on payments — with 5.3 million already in default and another 4.3 million just a few missed payments away.

Sen. Elizabeth Warren called it an “economic disaster in the making,” urging the Department of Education to act fast. But for borrowers, the more immediate question is simpler: What happens if my loans default — and can I fix it?

The short answer: yes, you can fix it.

Even if your student loans are in default, there are proven ways to recover, repair your credit, and get back into good standing. Here’s what default really means, why it’s spiking in 2025, and what steps you can take right now to get out.

What It Means to Default on Your Student Loans

Defaulting on your student loans means you’ve gone long enough without making payments that your lender or the federal government officially labels your debt as seriously past due.

For federal student loans, that happens after 270 days (about nine months) of missed payments without deferment, forbearance, or an active repayment plan. Once you hit that mark, your entire balance becomes due immediately — a process called acceleration — and your loan is transferred from your servicer to the Department of Education’s Default Resolution Group or a collection agency.

For private student loans, the timeline is shorter — usually 90 to 180 days of nonpayment, depending on the lender. Private loans don’t qualify for federal relief programs like income-driven repayment or rehabilitation, and lenders can move quickly to collections or even lawsuits.

In short: default turns your loan problem into a legal problem — one that can trigger collections, wage garnishment, and serious credit damage if left unaddressed.

What Happens When You Default on a Student Loan

Defaulting on your student loans can hit hard and fast. Here’s what to expect if it happens:

Your entire balance becomes due immediately. You lose access to flexible repayment options.

You lose federal benefits. That includes deferment, forbearance, new aid eligibility, and access to forgiveness programs.

Collection actions begin. Wage garnishment, tax refund seizure, or withheld Social Security benefits are common.

Your credit score drops. Many borrowers see a hit of 60 to 170 points, making it harder to qualify for loans, credit cards, or housing.

Additional fees pile on. Collection costs and interest can quickly inflate your balance.

The damage lingers. Default stays on your credit report for up to seven years.

That’s the tough part — but the good news is, you can reverse it. Through rehabilitation or consolidation, most borrowers can bring their loans back to good standing and start rebuilding credit within months.

Why Millions of Borrowers Are Facing Default in 2025

After years of pandemic relief, millions of borrowers are falling behind again as student loan payments resume. Reports from the Congressional Research Service show more than 5 million borrowers already in default and another 4 million close behind — what economists now call the “student loan default cliff.”

The End of Post-Pandemic Relief and the “Default Cliff”

When the post-pandemic relief period ended in fall 2024, many borrowers who hadn’t made payments in years suddenly had to restart them. Some managed to catch up, but millions didn’t — either because they couldn’t afford the new bills or never received clear guidance from their servicers.

With delinquency reporting and wage garnishments now back in play, defaults are climbing fast. Economists warn that this wave could squeeze consumer spending and credit access, particularly for families already stretched thin.

Policy Shifts Under the Big Beautiful Bill

The One Big Beautiful Bill Act (OBBB), signed in July 2025, made repayment even tougher for many. The law tightened borrowing limits, replaced familiar repayment plans like SAVE and REPAYE with new ones (RAP and revised IBR), and reduced access to relief programs.

At the same time, staffing cuts at the DoE left over 1 million IDR applications pending — meaning many borrowers are still waiting for payment adjustments that could prevent default.

Why Borrowers Are Falling Behind

Beyond policy, everyday economics are making repayment harder than ever:

Rising costs: Inflation and high housing prices are squeezing budgets.

Administrative delays: Servicer confusion and IDR backlogs leave many unsure of their payment status.

Borrower fatigue: After years of pauses and shifting policies, some borrowers simply checked out.

Defaults spreading: Even high-credit borrowers are missing payments, often prioritizing essentials over student loans.

The bottom line: the system restarted before it was ready, and millions are paying the price. But while the headlines sound grim, default isn’t permanent — there are still clear, proven ways to fix it and start fresh.

How to Fix a Defaulted Student Loan

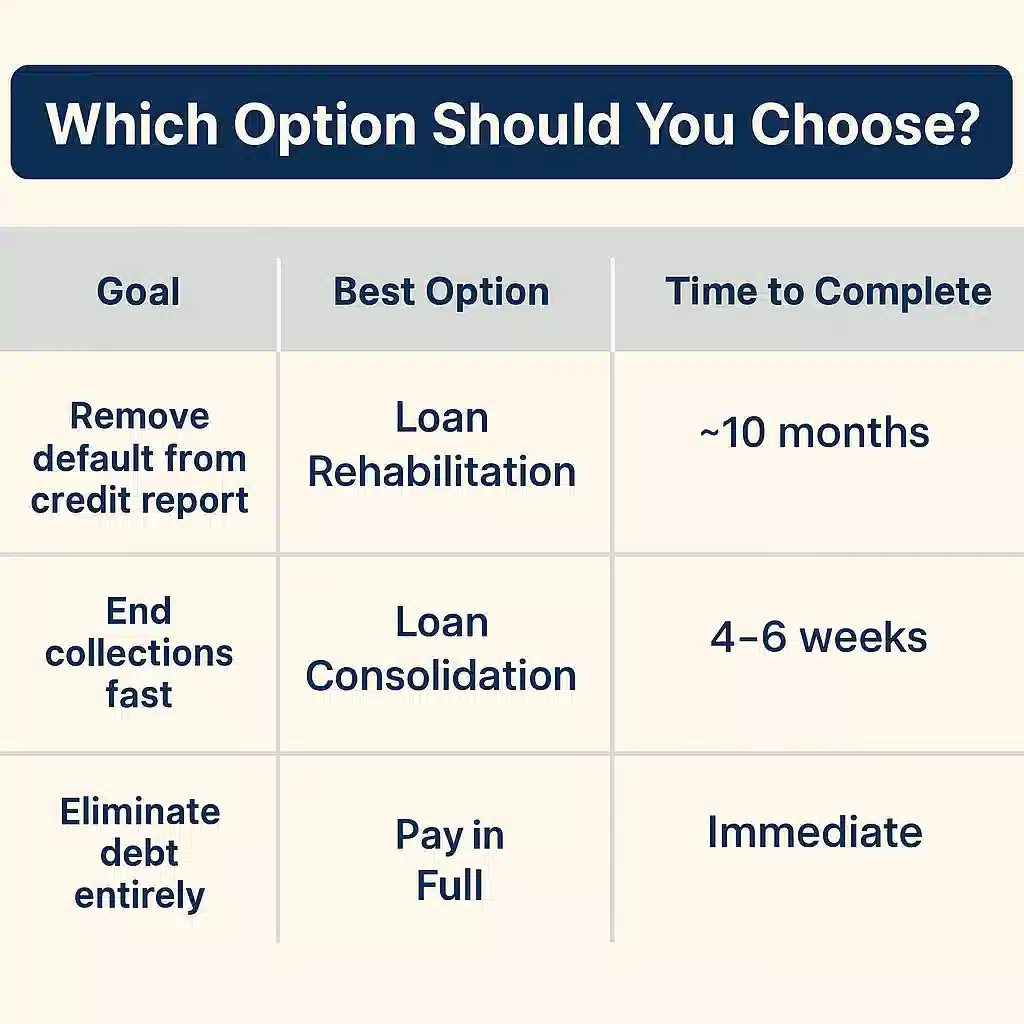

Default feels final, but it’s not. The federal system gives borrowers a few clear paths to recover, and most people can get back on track within months — not years.

The best way to fix student loan default depends on your situation, but for federal loans, there are three main options: rehabilitation, consolidation, and paying in full. (Private loans work differently — we’ll cover those next.)

Option 1: Loan Rehabilitation (Best for Credit Repair)

Loan rehabilitation is usually the best fix if you want to remove the default mark from your credit report and regain federal loan benefits.

You’ll make nine on-time monthly payments within ten months — typically around 15% of your discretionary income. If that’s too high, your servicer can set a lower amount (sometimes as little as $5) based on your financial situation.

Once you’ve made all nine payments:

Your loans are taken out of default and reassigned to a new servicer.

Collection actions like wage garnishment and tax refund seizures stop.

You regain eligibility for deferment, forbearance, forgiveness, and new aid.

The default is removed from your credit report (though late payments before default stay).

Best for: Borrowers who want to rebuild credit and have a steady enough income to make small monthly payments.

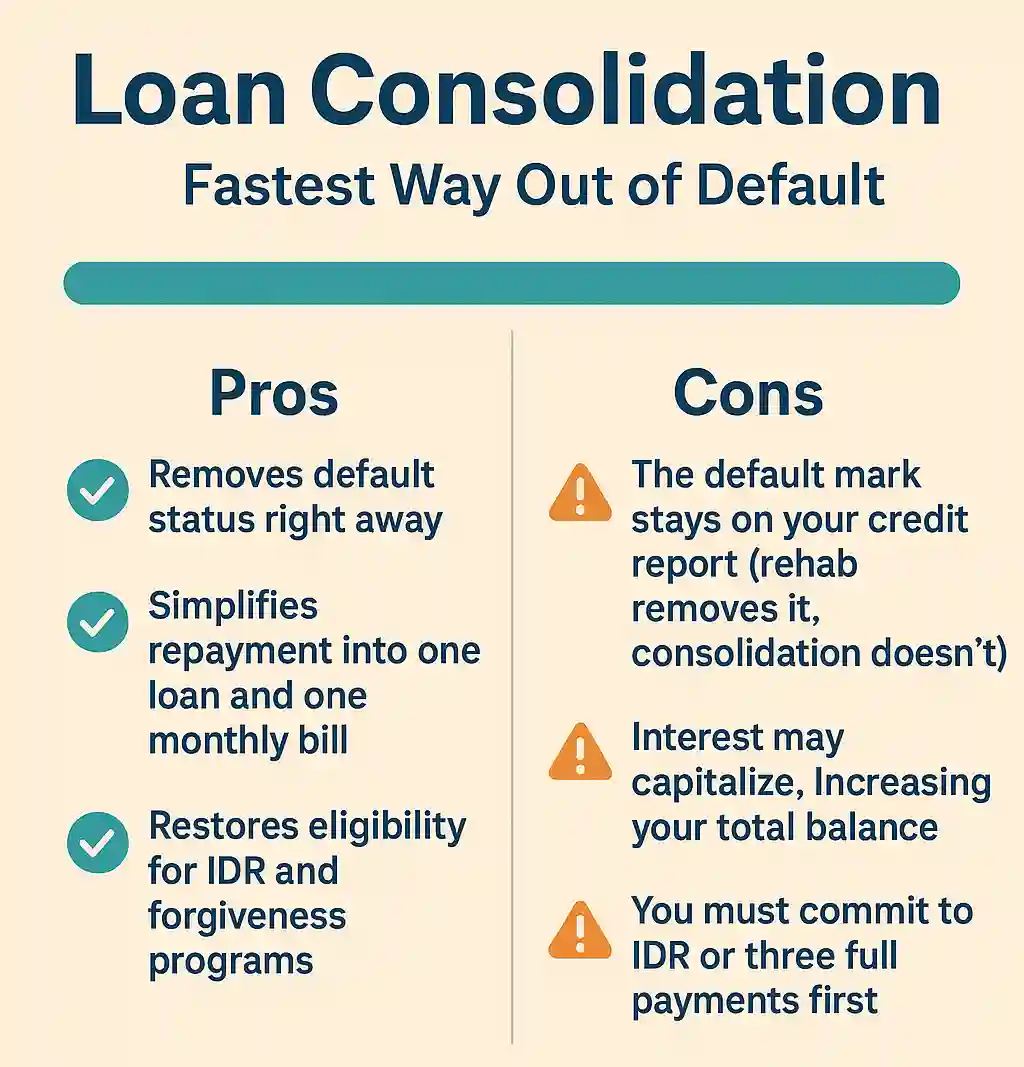

Option 2: Loan Consolidation (Fastest Way Out of Default)

If you need to get your loans out of default quickly, consolidation is faster. You’ll combine one or more defaulted federal loans into a new Direct Consolidation Loan, instantly bringing your account current.

To qualify, you must either:

Agree to repay the new loan under an income-driven repayment (IDR) plan, or

Make three consecutive, on-time, full monthly payments before consolidating.

Once approved, your new loan pays off the old ones, ending collections immediately.

Best for: Borrowers who need a fast fix or are facing wage garnishment or collection pressure.

Quick tip: If you plan to apply for a mortgage or new credit soon, consider rehabilitation first — it offers better long-term credit recovery, even if it takes longer.

Further Reading: Not sure whether rehabilitation or consolidation makes more sense for your situation? Check out our detailed comparison: Rehabilitation or Consolidation for Defaulted Student Loans? — it breaks down the pros, cons, fees, and long-term credit impact of each option.

Option 3: Paying the Loan in Full (Rare but Instant Fix)

If you can afford it, paying your defaulted loan in full is the quickest way to clear the debt and end all collection activity. Once paid, your loan is immediately considered current.

However, this isn’t realistic for most borrowers — and it doesn’t remove the default from your credit report. It simply stops the bleeding.

Best for: Borrowers with access to large funds (like an inheritance or settlement) who want to close the chapter on student debt entirely.

Once you’ve fixed the default, the next step is keeping it from happening again. The good news: that’s much easier — and it starts with setting up a repayment plan that actually fits your income.

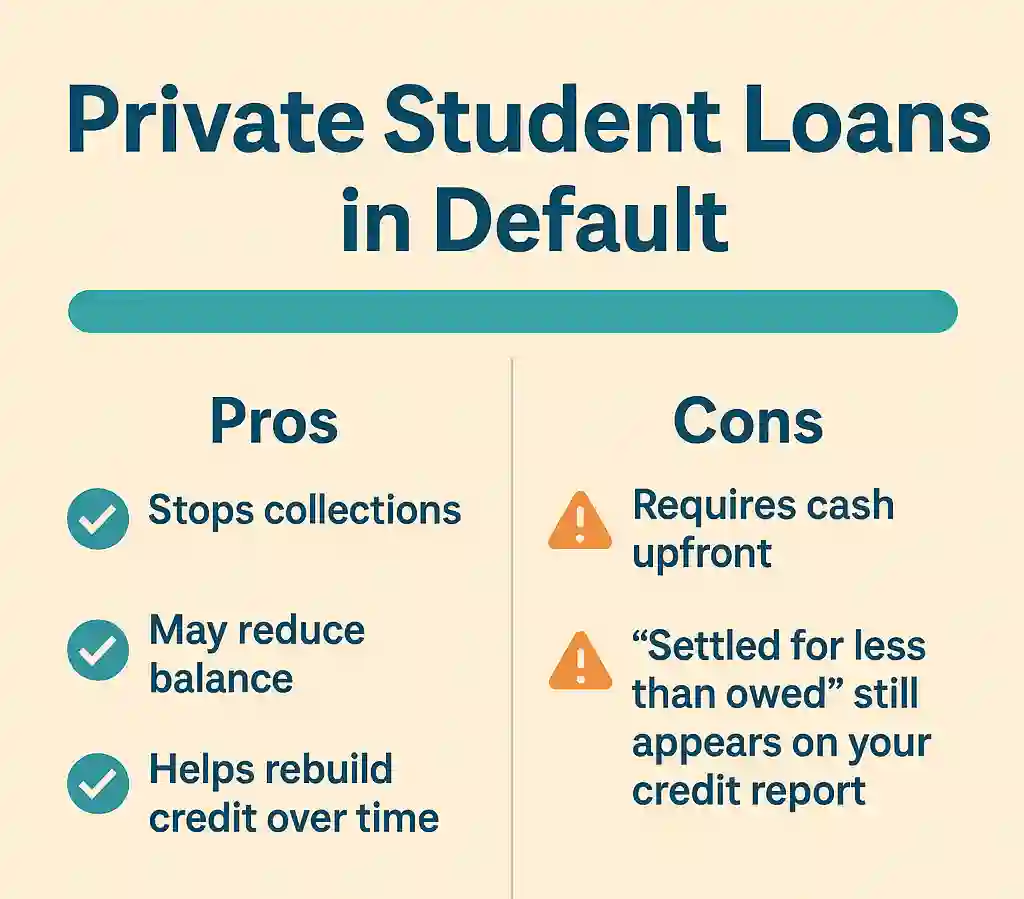

Private loans don’t follow federal rules, and they don’t offer rehabilitation. Most private lenders consider a loan in default after 90–180 days of missed payments.

If your private loan defaults:

Contact your lender immediately — many will negotiate new repayment terms to avoid litigation.

You can request a settlement, often paying 50–70% of the total balance in a lump sum or short-term plan.

Be aware that lawsuits are common. Private lenders can sue to garnish wages or seize assets (depending on state law).

Once you’ve fixed the default, the next step is keeping it from happening again. The good news: that’s much easier — and it starts with setting up a repayment plan that actually fits your income.

How to Avoid Student Loan Default Again

Once your loans are back in good standing, the goal is simple: keep them that way. The best way to avoid default again is to make your payments affordable, automatic, and always up to date — even when life gets messy.

Here’s how to stay out of the red for good:

1. Enroll in an Affordable Income-Driven Repayment Plan (IDR)

If your payments feel impossible, that’s a sign you’re probably on the wrong plan.

Switching to an IDR plan keeps monthly payments tied to your income and family size — not your loan balance.

As of 2025, the IBR plan and the new RAP are the most reliable options. The SAVE Plan is still in legal limbo, so new enrollments are limited, but IBR and RAP remain open and safe choices.

Enrolling in an IDR plan can:

Lower your payment to as little as $0 per month if your income qualifies.

Keep your account in good standing even if you’re earning very little.

Keep you eligible for forgiveness programs down the road.

If you’re unsure where to start, visit Studentaid.gov/idr and use the Loan Simulator to compare plans.

Related: Federal Student Loan Repayment Plan Options and Strategy — This article breaks down every repayment plan (SAVE, IBR, PAYE, and more) and explains how to pick the one that minimizes interest and maximizes forgiveness.

Pro tip: If your servicer hasn’t processed your IDR application yet, make at least one small monthly payment anyway — it helps prevent delinquency while you wait through the backlog.

2. Set Up Auto-Pay and Track Your Loan Status

It sounds obvious, but automation is the easiest way to prevent missed payments. Setting up auto-pay through your loan servicer ensures payments are made on time, every time — and you might even get a small interest rate discount (usually 0.25%).

Don’t just set it and forget it, though. Log in to your StudentAid.gov dashboard at least once a month to:

Check your payment history

Verify your servicer hasn’t changed (it happens more than you’d think)

Review your IDR recertification dates

Even a quick five-minute check can catch errors before they spiral into delinquency.

3. Recertify on Time (Even if the DOE Is Backlogged)

The Department of Education is still digging out from a massive 1.1 million IDR application backlog, which means your paperwork could sit for months. That’s why it’s critical to recertify early — ideally 60 to 90 days before your annual deadline.

If your income or family size changes, recertify right away to keep your payments accurate. Missing your recertification date can cause your payments to jump or your IDR plan to lapse, putting you back on a higher standard plan — the fastest path back to delinquency.

Bottom Line: Consistency Beats Perfection

Avoiding default isn’t about being perfect — it’s about staying consistent. Pick a repayment plan that fits your life, automate what you can, and keep tabs on your loans at least once a month.

Once you’ve climbed out of default, the hard part’s over. From here, it’s all about maintaining progress — and knowing where to get help before small problems turn into big ones.

Final Take

Defaulting on your student loans can feel like the end of the road — but it’s not. It’s a detour, not a dead end.

Millions of borrowers have been where you are right now and made it out. Whether you choose rehabilitation to clean up your credit or consolidation for a faster fix, the key is to take action before collections get worse. Once you’re out of default, enrolling in an affordable income-driven repayment plan and setting up auto-pay are your best defenses against sliding back.

If your loans are already in default, don’t ignore the problem — you can recover faster than you think. Check your status onStudentAid.gov, call your servicer, and start the process that fits your situation. Every payment, every step, moves you closer to financial stability and future forgiveness.

Ready to get back on track? Schedule a one-on-one consultation with Pedro Gomez, CFP®, and get a personalized plan to fix your default, choose the right repayment strategy, and rebuild your financial future — faster.

Federal student loans typically go into default after 270 days (about nine months) of missed payments without deferment, forbearance, or an active repayment plan. Private lenders often declare default sooner, usually after 90 to 180 days depending on the loan contract.

For federal loans, you can check your status on Studentaid.gov, which tracks your loan standing. For private loans, you need to monitor your loan servicer’s communications or check your credit report for defaults or collection entries.

The primary ways are loan rehabilitation, consolidation, or settlement. Rehabilitation requires nine on-time monthly payments and removes default status. Consolidation pays off the defaulted loan with a new loan, and settlement involves negotiating payoffs with lenders or collectors.

A federal student loan default typically stays on your credit report for seven years. However, successful rehabilitation removes the default status sooner, improving your credit profile more quickly.

Discharge of defaulted student loans is rare. It is usually granted only in cases of total and permanent disability, school closure, or very limited bankruptcy conditions. Regular discharge through bankruptcy is generally not allowed.

Pedro Gomez is the new Student Loan Sherpa and a Certified Financial Planner™ with over a decade of experience helping clients navigate complex financial decisions. He is the founder of Global Financial Plan, where he writes about international living, geoarbitrage, and strategies for retiring young, and also leads Brickell Financial Group, a registered investment advisory firm focused on accelerating financial freedom.

Pedro is the architect behind the “12 Levels of Financial Freedom” framework and blends student loan strategy with long-term planning, tax efficiency, and investing. His work is especially geared toward upwardly mobile professionals, entrepreneurs, and those looking to design a life beyond the default path.

By now, it’s obvious that the Trump administration’s efforts to expand Immigration and Customs Enforcement activities go far beyond enforcing federal immigration policy. The near-daily stories of inhumane detainment conditions, open violence against citizens and noncitizens alike, wanton civil rights violations, and purposeful shielding of these abuses from any form of public accountability lay bare that President Trump is now using ICE as a key component for advancing his administration’s hateful agenda.

This context is essential to evaluate why the administration has sung such a different tune with the advertised $60,000 student loan forgiveness offers to new ICE recruits, compared to the normal song and dance about how higher education is evil incarnate. Trump and his political allies didn’t suddenly discover the societal benefits of affordable education, as evidenced by his simultaneous efforts to strip loan forgiveness pathways from those who are deemed obstructors to Trump’s political goals. What’s clear is that federal student loan forgiveness is now a poverty draft, coercing increased ICE and military enlistment from among those experiencing economic desperation.

Weaponizing educational debt to fuel armed forces conscription from lower-income individuals is essentially socioeconomic hostage taking. It deprives people of their agency in choosing whether conscription is truly the career and life pathway they desire by forcing the decision as a survival tactic, especially when nearly half the country is approaching an economic recession deliberately caused by Trump’s policies.

A History of Weaponizing College Affordability

The easiest way for an authoritarian regime to maintain a highly militarized state is to make enlistment the only means of socioeconomic survival for the masses. This is exactly why the Trump administration is promoting student loan forgiveness for ICE recruits while curtailing eligibility for Public Service Loan Forgiveness. By passing the reconciliation bill that nearly tripled ICE’s budget while restricting Pell Grant eligibility for some students and cutting back basic needs programs like food stamps and Medicaid, congressional leaders have identified themselves as active participants in this strategy.

Though Trump’s tactics are an unprecedentedly naked attempt to weaponize student loan relief in the service of authoritarianism, this is a foundational concept in federal higher education policy that he’s taking the opportunity to exploit. The Servicemen’s Readjustment Act of 1944, the first federal educational assistance program for veterans, and most follow-up educational assistance programs were more focused on rewarding military service in already-declared conflicts than using benefits as a recruitment draw.

That shift came with the larger 1960s push to align higher education with the Cold War. California’s Master Plan of 1960 provided an opening for later attacks on college affordability, because it codified into public policy the idea that some types of institutions were worth attending more than others, mainly by segregating various types of educational experiences offered by different institutions. Later in the decade, then–California governor Ronald Reagan slashed public university budgets, in this way punishing students for antiwar protests. Reagan’s camouflaging of draconian education funding cuts as a necessary tool to combat the “filthy speech movement” became the groundwork for today’s deep inequality across all levels of the educational system.

Over the next several decades, federal and state policymakers abandoned their responsibilities to fund public higher education, which has strengthened the ties between college (un)affordability and militarization. In 2022, 20 Republican House members—14 of whom are still in office—wrote a joint letter to then-president Biden expressing concern that his efforts to provide widespread student loan forgiveness would harm the ability of the military to use higher educational benefits as a recruitment tool.

Last fall, 48 percent of 16- to 21-year-olds surveyed by the Department of Defense identified “to pay for future education” as a main reason they would consider joining the armed forces. This was the second-most common reason expressed in the survey, behind only “pay/money.”

Student Loan Forgiveness Is Not Siloed Public Policy

Public policy is rarely siloed into neat categories, and we are now experiencing the widespread consequences of allowing an inequitable and unaffordable higher education system to exist for so long in the United States. Trump isn’t the only federal policymaker endorsing this strategy, but he is the primary beneficiary. The more people willing to join ICE’s march toward martial law or forced to join ICE due to socioeconomic necessity, the easier it is for Trump to fully embrace authoritarianism and stay in power past January 2029.

This is the framing that should be used in every policy conversation about student loan forgiveness moving forward, not just for the offers given to new ICE recruits. These actions are not distinct or separate from the administration’s federalizing of the National Guard, ICE’s vast increase in weapons spending or Trump’s public consideration of invoking the Insurrection Act to deploy more troops to U.S. cities; they’re a vital complement. Ransoming access to an affordable higher education, along with its associated socioeconomic benefits, based on how willing someone is to inflict terror on immigrant communities or any other population that the administration deems undesirable, is a deliberate tactic to build an authoritarian military state.

Ideally, the current scenario facing higher education will end the usual hemming and hawing from policymakers about universal student loan forgiveness or tuition-free higher education being too expensive. Are the cost savings from not offering widespread forgiveness truly worth militarizing the country against the estimated 51.9 million immigrants living in the U.S., including more than 1.9 million immigrant and undocumented higher education students? Is appeasing Trump’s desire to play dictator dress-up so vital that policymakers feel compelled to willingly eradicate recent progress in national college affordability, discourage or outright bar international students from coming to learn in the United States, and shrink the economies of every state and congressional district due to the loss of international students?

State Legislatures Are the Last Line of Defense

The Trump administration is desperate to expand domestic militarization through ICE, as evidenced by advertisements on popular media streaming services and during nationally televised football games, public commitments to keep paying ICE agents as roughly 1.4 million federal workers go without pay during the government shutdown and the elimination or loosening of recruitment and training requirements for new ICE agents in relation to their age, physical fitness and ability to speak Spanish. As the Trump administration through ICE utilizes every available tool to further its authoritarian agenda, policymakers and institutions must use every available tool to combat said authoritarianism.

State legislatures wield vast amounts of legal authority over education policy in comparison to the federal government. However, that authority is useless if states capitulate or are otherwise unwilling to use that authority to protect their education systems and their larger communities.

Efforts like Connecticut’s new statewide student debt forgiveness program, California’s prohibition on campus police departments providing personal student information for immigration enforcement purposes and Colorado’s adoption of a new state law requiring public campuses to limit federal agents’ access to campus buildings are all welcome ways that state policymakers can fight back against ICE.

These efforts must be expanded to more states as ICE continues to ramp up its domestic terrorism and congressional leadership remains content to abandon its constitutional responsibilities to hold the executive branch in check. For institutions, advocates and concerned community members, resources available through the Presidents’ Alliance on Higher Education and Immigration and its Higher Ed Immigration Portal, and from the Immigrant Legal Resource Center, provide essential guidance on how to act in protecting immigrants and their families.

Student loan forgiveness, and the larger concept of an affordable and equitable higher education, could now be a matter of life and death for millions of people. The traditional willingness of policymakers to resist supporting higher education during times of economic surplus, while eagerly cutting educational funding at the first sign of economic distress, has now imperiled American democracy. Every image of ICE committing authoritarian violence is a stark call for policymakers to ask themselves what they value more: the fiscal savings of making no meaningful effort to address the more than $1.6 trillion owed in student debt, or American democracy itself.

Christian Collins is a policy analyst with the education, labor and worker justice team at the Center for Law and Social Policy, a nonprofit organization focused on reducing poverty and advancing racial equity.

After two days of talks, Department of Education officials have made it clear that they won’t budge over some new student loan regulations.

Specifically, the department has said it won’t negotiate its proposed definition of a professional program, at least for now. That definition limits the category to 10 specific degrees, including law, medicine and theology.

“At this point, we would like to keep the language where it is,” Tamy Abernathy, the department’s director of policy coordination, said Tuesday morning. “It’s not an exhaustive list, but it is fixed at this point in time, with the caveat that if it needs to be negotiated at a future date, it would be.”

If the department stands firm on this position, dozens of health-care graduate programs, like clinical psychology and occupational therapy, would not be on the list and could be subject to a $20,500 annual cap on student loans. If these programs were to be deemed professional, federal student loans would be capped at $50,000 a year and $200,000 over all. (Graduate programs are capped at $100,000 over all.)

With a lower cap, the programs could see steep enrollment drops and some might have to close, experts say. But members of the advisory committee tasked to weigh in on the department’s proposals pushed back over the first two days, and some are hopeful that the tone of conversation will shift for the remainder of the week.

At the very end of Tuesday’s meeting, committee members submitted their own definition for professional programs, which has not been released to the public but will be discussed Wednesday. The committee is scheduled to meet through Friday and then for another week in November before voting on the regulatory changes. If the committee doesn’t reach unanimous consensus, the department can propose its own draft regulations, which will be subject to public comment.

Education Under Secretary Nicholas Kent said in a statement to Inside Higher Ed shortly after Tuesday’s meeting that the department is continuing to negotiate in good faith but is aiming “to curb excessive graduate student borrowing in the federal student loan program.”

“At this time, we remain persuaded that limiting the list of eligible programs to those defined in current regulation—while remaining open to expanding that list through future rule making—is the better approach for both students and taxpayers,” Kent said. “We are committed to working with negotiators and the public to hear and thoughtfully consider differing perspectives.”

This round of rule making is just one part of the department’s larger effort to quickly interpret Congress’s sweeping overhaul of federal student aid through the One Big Beautiful Bill Act, which was signed into law in July. When it comes to student loans in particular, ED has to clarify each of the law’s provisions and implement them before the July 1, 2026, deadline.

Higher ed experts say that heated debate over how to define professional versus graduate programs reflects how the loan caps are likely one of OBBBA’s most consequential changes for the sector.

The department’s “limited list of programs designated as professional could have big implications for students,” said Karen McCarthy, vice president of public policy for the National Association of Student Financial Aid Administrators. “It could push some students into the private student loan market, which has fewer borrower protections than federal student loans, or limit access for [others] who are unable to obtain private loans. This could lead to lower numbers of graduates in highly critical career fields such as mental health, nursing and education.”

An Appetite for Change?

The department’s latest proposal, as of Tuesday, was similar to the existing statutory definition cited by Congress in the new legislation, which says a professional program must prove a student has the skills necessary beyond a bachelor’s degree to pursue a certain licensed profession.

But the statutory definition from the Higher Education Act of 1965 includes a nonexhaustive list of examples; the department’s proposal is finite. The HEA definition says, “Examples of a professional degree include, but are not limited to,” whereas the department’s proposal says, “These programs are designated as professional” and then lists 10 degrees: in pharmacy, dentistry, medicine, osteopathy, law, optometry, podiatry, veterinary medicine, chiropractic medicine and theology.

Abernathy explained that despite removing the phrase “including but not limited to,” the department’s proposal is not exhaustive, as it gives the secretary flexibility to designate additional professional degrees through rule making in the future. So while the department does not “have an appetite” to change the definition now, that doesn’t mean it wouldn’t be able to later, she said.

But several committee members were not satisfied with that explanation. Scott Kemp, a student loan advocate for the Virginia higher ed council and the committee member representing state officials, said he came to the table with the understanding that the department was open to changing that list now.

“We’re already in rule making right now, and there’s an opportunity to do that here,” he said. “I guess the understanding is that that door has been closed. But for our constituents who disagree with this list and have been giving us an earful about it, what would it take to have the secretary designate a rule-making process to discuss the list?”

Andy Vaughn, president of a for-profit graduate school in California and the representative for proprietary institutions, said that in his view the most “glaring omission” from the list is mental health practitioners.

“We rarely have a week in our country where some national story about mass violence doesn’t hit our news feeds, and every time that happens, mental health is the foundational, seminal place that we point to,” Vaughn said. “So including mental health license programs—one way or the other—is really critical, because this is going to decimate the pipeline of mental health professionals.”

In a later interview with Inside Higher Ed, he added that while he agrees the overall price of tuition is too high, it’s “really hard” to get certain high-cost programs, especially those that take three or more years, under the $100,000 limit for programs that are not deemed professional.

And even if the department were to come back to the table to amend the list at a later date, he believes it would be “too late,” as enrollment for many high-demand programs would have already dramatically declined.

“It’s hard to say with certainty what exactly happens if professional designation is not granted,” he said. “But I can tell you with certainty it’s not going to increase the pipeline.”

Vaughn, Scott and eight other committee members representing taxpayers, state officials and various types of universities broke out into a private caucus twice during Tuesday’s meeting to further discuss the definition. By the end of the day, they’d drafted a new proposal that will drive the conversation with department officials tomorrow.

“The department has said they’re willing to have this conversation, but I believe we must,” Vaughn said.

At least a quarter of students across a broad range of graduate and professional programs could need private loans, which tend to come with higher interest rates, in order to pay for their education once new caps on federal loans take effect next summer, multiple studies show. For some, the loans could become so costly as to make earning a master’s or doctoral degree unattainable.

Currently, this group can borrow federal loans up to the total cost of attendance thanks to a program known as Grad PLUS. But starting July 1, students will max out at either $20,500 or $50,000 per year depending on whether they enroll in a graduate or professional program, respectively. And those in graduate programs will only be able to take out $100,000 over all, while students in professional programs will be limited to $200,000. Congress made the changes as part of the One Big Beautiful Bill Act, which passed earlier this summer.

The caps mean that the median borrower in four of the nine largest professional programs likely will need to find other financing to pay tuition bills, according to a recent analysis from the Postsecondary Education and Economics Research Center at American University. Borrowers in the 75th percentile exceed the cap in six of the nine fields.

And it’s not just the most costly doctoral programs such as medicine and dentistry in which students will face such a challenge, PEER notes. Out of the 30 master’s degree programs with the highest loan volume, 50 percent of students exceed the cap in nearly half of them.

Many of these students could struggle to find a private lender to make up the difference, potentially forcing them to drop out or not enroll in the first place, policy experts at PEER and other research groups say. And even if a student finds a lender, taking out a private loan could lead to steep, sometimes predatory, interest rates that take decades to pay off. (Research shows that low-income individuals particularly struggle to secure private financing because of a range of factors such as low credit scores, a lack of assets or an inconsistent flow of income.)

Before this new law, “students could have just filled out their FAFSA, applied for loans through the Department of Education and been able to borrow up to the full cost of attendance of their program,” said Jordan Matsudaira, director of the PEER Center and a former deputy under secretary at the Department of Education.

But now, for upward of a quarter of graduate students, it likely won’t be that simple.

“I think that will come as a surprise to a lot of people,” he said.

Can Private Lenders Fill the Gap?

Other researchers at Urban Institute and Jobs for the Future have also crunched the numbers on the loan caps and reached similar findings.

Jobs for the Future estimated in a report released last month that if this loan cap had been in place for the 2019–20 graduating class, roughly 38 percent of graduate borrowers would have needed to take out more loans beyond the cap. And thanks to the limit, the federal government would have issued $9.7 billion less in loans—a decrease of about 28 percent, according to the report.

Urban also used data from 2019–20 but broke it down by program, finding that dentistry would have the largest share of students exceeding the cap. About 56 percent would have exceeded the annual limit, and 58 percent blew through the aggregate cap. Other programs with a high share of students that could be pushed into the private market include medicine, at 41 percent, a master’s in public health, at 29 percent, and a master’s in fine arts, at 26 percent.

Policy experts on both sides of the political aisle tend to agree that the student debt crisis needs to be addressed. But unlike conservative lawmakers and analysts who believe these caps are necessary in order to lessen student debt and encourage colleges to lower costs, some researchers worry the limits are too aggressive and don’t account for nuances like a program’s return on investment.

“The kind of pain involved here is a little bit bigger than it needed to be to rein in the most egregious abuses in the system,” Matsudaira said. “The better approach over all would have been to adopt an approach where different fields of study had different limits that were scaled with borrowers’ ability to repay.”

Some questions about how the loan limits will work and which programs they’ll apply to will be answered later this month when the Education Department starts to work through the rule-making process to carry out the law’s provisions. Representatives from nursing, aviation and social work have already started to speak out about why their programs should be considered professional degrees and therefore be eligible for the higher cap.

“In today’s economy, the majority of graduate education is practical and workforce-aligned, preparing students for jobs in health care, education, counseling, technology and much more,” Stephanie Giesecke, a representative of the National Association of Independent Colleges and Universities, said at a public hearing in August. “The definition that is too narrow risks excluding programs that are vitally important to communities and employers nationwide.”

Like Matsudaira, Ethan Pollack, a senior director of policy at JFF, said that while he sympathizes with the Republican diagnosis that debt is too high, he probably would have gone about addressing it a different way. But rather than suggesting changes to the cap itself, JFF’s report looked at the financial impact on borrowers and suggested ways that institutions, the government and private lenders can adjust in response.

One key recommendation was the use of outcomes-based financing for private loans, which would base payments in part on borrowers’ earnings after graduating. Pollack said that this approach could help students who lack strong credit histories or cosigners still pursue well-paying degrees like a juris doctorate.

But current regulations, like requiring a bank to disclose a flat annual percentage rate, or APR, when offering a loan, make it difficult for some private vendors to explore new models like outcomes-based financing, he explained. If the government were to build on the recent legislation by amending current regulations and introducing new guardrails for private lenders, Pollack added, the OBF model could make nonfederal loans more affordable for borrowers of all backgrounds.

“The federal government, in some sense, is stepping on the gas and the brake at the same time,” he said. “They’re saying that they want the private market to be stepping up, but at the same time, the federal government is one of the obstacles to the private market being able to step up in the way that we would all like them to, which is to be offering financing with much more student-friendly terms.”

Matsudaira, on the other hand, was more skeptical.

“The big question is whether the private sector is really going to be able to come in and fill a hole that big,” he said. “And even if they do, how long does it take for them to spin up to be able to do those kinds of things?”

Todd S. Nelson rose from academic beginnings—a B.S. from Brigham Young University and an MBA from the University of Nevada, Reno—to dominate the for-profit higher education space. Over nearly four decades, Nelson has amassed vast personal wealth leading University of Phoenix, Education Management Corporation (EDMC), and Perdoceo Education, even as each institution left embattled students and regulatory fallout in its wake.

Under Nelson’s leadership, Apollo Group (parent of University of Phoenix) mountains of revenue—$2.2 billion and over 300,000 students by 2006—coincided with a $41 million payday in that year alone. He resigned amid pressure over deceptive admissions practices.

Nelson’s move to EDMC in 2007 triggered another enrollment explosion—from 82,000 to over 160,000 students by 2011—propelled by federal student aid. Annual revenues reached nearly $2.8 billion, even as employees were alleged to be encouraged to enroll “anyone and everyone” to meet quotas. This aggressive focus on recruitment came with enormous personal compensation—approximately $13.1 million annually—while students endured mounting debt and dwindling outcomes.

A 2015 landmark settlement exposed EDMC’s alleged violations under the False Claims Act. The Justice Department accused the company of operating as a “recruitment mill,” illegally funneling federal funds through false certifications. EDMC agreed to pay $95.5 million in damages and forgive more than $102 million in student loans, affecting about 80,000 former students—averaging around $1,370 per student.Internal documents and court filings paint a grim picture: incentive-based pay for recruiters, breach of fiduciary duties, and a business model the trustee called “fundamentally fraudulent.”

Nelson’s chapter at Career Education Corporation (later Perdoceo) echoed the same script. Campuses shuttered, including Le Cordon Bleu and Sanford-Brown, left students stranded with untransferable credits—and yet Nelson’s compensation remained soaring. In 2019, he earned $7.4 million and held about $12 million in equity.

Whistleblower accounts from inside Perdoceo’s operations are damning. One former recruiter described pressure to enroll students “by any means necessary,” including coercive calls and emotional manipulation—often targeting vulnerable applicants with low income or lacking basic readiness. Despite those practices, Perdoceo reaped profits, with Nelson publicly touting revenue growth even as the Department of Education issued a formal notice in May 2021: thousands of borrower defense claims were pending against the company, alleging misrepresentations on credits, employment prospects, and accreditation.

Further regulatory investigations deepened through early 2022, focusing on recruiting, marketing, and financial aid practices—yet no executive accountability has followed.

The narrative that emerges is stark: Todd S. Nelson repeatedly led institutions to profit-fueled expansion using students’ federal dollars, while suppressing outcomes and exposing students to debilitating debt. Lawsuits, settlements, and investigative reports expose deceptive enrollment practices, false claims, and regulatory violations—but the executives—including Nelson—walk away with wealth and are rarely held personally responsible.

Sources

Wikipedia: Todd S. Nelson—compensation figures and resignation amid scrutiny.

TribLIVE: Allegations of “anyone and everyone” being enrolled to meet quotas under Nelson’s reign at EDMC.

Career Education Review: Insights on quality decline amid enrollment growth at EDMC and Perdoceo.

Department of Justice and NASFAA: 2015 EDMC settlement—$95.5 million damages, $102 million in loan forgiveness for hundreds of thousands.

Bankruptcy court filings: Allegations of fraudulent business model and incentive-driven recruitment.

Republic Report & USA Today: Whistleblower testimony on Perdoceo’s predatory recruiting tactics.

After a three-year pause prompted by the pandemic, the clock on student loan repayments suddenly started ticking again in September 2023, and forbearance ended last September. For millions of borrowers like Shauntee Russell, the resumption of payments marked a harsh return to financial reality.

Russell, a single mother of three from Chicago, had received $127,000 in student loan forgiveness through the SAVE program, and had experienced profound relief at having that $632 monthly payment lifted from her shoulders. SAVE exemplified both the transformative power of debt relief and the urgent need to continue this fight — but now SAVE has been suspended.

Such setbacks cannot be the end of our story, as I document in my forthcoming book. The resumption of loan payments, while painful, must serve as a rallying cry rather than a surrender. We stand at a critical juncture. The Supreme Court’s devastating blow to former President Biden’s initial forgiveness plan and the ongoing legal challenges to programs like SAVE have left 45 million borrowers in a state of financial limbo. The fundamental inequities of our higher education system have never been more apparent.

Black students graduate with nearly 50 percent more debt than their white counterparts, while women hold roughly two-thirds of all outstanding student debt — a staggering $1.5 trillion that continues to grow. These aren’t just statistics; they represent systemic barriers that prevent entire communities from achieving economic mobility.

Related: Interested in innovations in higher education? Subscribe to our free biweekly higher education newsletter.

The students I interviewed while reporting on this crisis reveal the human cost of inaction. They include Maria Sanchez, a nursing student in St. Louis who skips meals to save money and can only access textbooks through library loans.

Then there is Robert Carroll, who gave up his dorm room in Cleveland and now alternates between friends’ couches just to stay in school.

These students represent the millions who are working multiple jobs, sacrificing basic needs and seeing their dreams deferred under the weight of financial pressure.

Yet what strikes me most is their resilience and determination. Despite these overwhelming obstacles, these students persist, driven by the same belief that motivated civil rights leaders like Congressman Adam Clayton Powell Jr. — that education is the pathway to economic empowerment and social justice.

The current political landscape, with Donald J. Trump’s return to the presidency and a Republican-controlled Congress, presents unprecedented challenges. Plans to dismantle key borrower protections and efforts to eliminate the Department of Education signal a dark period ahead for student debt relief.

But history teaches us that progress often comes through sustained grassroots organizing and innovative policy solutions at multiple levels of government and society.

Universities must step up with institutional relief programs, as my own institution, Trinity Washington University, did when it settled $1.8 million in student balances during the pandemic.

The Black church, which has long understood the connection between education and liberation, continues to provide crucial support through scholarship programs. Organizations like the United Negro College Fund, the Thurgood Marshall College Fund and the National Association for Equal Opportunity in Higher Education remain vital pillars in making higher education accessible.

Still, individual, institutional and state efforts, while necessary, are not sufficient. We need comprehensive federal action that treats student debt as what it truly is: a civil rights issue and a moral imperative. The magnitude of the crisis — it affects Americans across every congressional district — creates unique opportunities for bipartisan coalition building.

Smart advocates are already reframing the narrative by replacing partisan talking points with economic arguments that resonate across ideological lines: workforce development, entrepreneurship and American competitiveness on the world stage.

When student debt prevents nurses from serving rural communities, teachers from working in underserved schools and young entrepreneurs from starting businesses, it becomes an economic drag that affects everyone.

The path to federal action may require creative approaches — perhaps through tax policy, regulatory changes or targeted relief for specific professions — but the political mathematics of 45 million impacted voters ultimately makes comprehensive action not just morally necessary, but politically inevitable.

Student debt relief is not about handouts — it’s about honoring the promise that education should be a ladder up, not an anchor weighing down entire generations; it’s about ensuring that Shauntee Russell’s relief becomes the norm, not the exception. The fight is far from over.

The young activists I met at the March on Washington 60th anniversary understood something profound: Their debt is not their fault, but their fight is their responsibility. They carry forward the legacy of those who came before them who believed that access to education should not depend on one’s family wealth, and that crushing debt should not be the price of pursuing knowledge.

The arc of history still bends toward justice — but in this era of political resistance, we must be prepared to bend it ourselves through sustained organizing, innovative policy solutions and an unwavering commitment to the principle that education is a right, not a privilege reserved for the wealthy.

The resumption of payments is not the end of this story. It’s the beginning of the next chapter in our fight for educational equity and economic justice. And this chapter, like those before it, will be written by the voices of the millions who refuse to let debt define their destiny.

Jamal Watson is a professor and associate dean of graduate studies at Trinity Washington University and an editor at Diverse Issues In Higher Education.

The Hechinger Report provides in-depth, fact-based, unbiased reporting on education that is free to all readers. But that doesn’t mean it’s free to produce. Our work keeps educators and the public informed about pressing issues at schools and on campuses throughout the country. We tell the whole story, even when the details are inconvenient. Help us keep doing that.

{kind=link}